The data behind this list comes from Dakota Marketplace, the global private markets intelligence platform used by thousands of investment professionals to research LPs, GPs, and private companies. Built by fundraisers for fundraisers, Dakota Marketplace delivers complete, accurate, and daily-updated intelligence across every allocator channel, from family offices and RIAs to sovereign wealth funds and public pensions. Learn More | Book a Demo

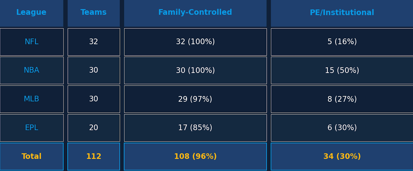

108 of 112 professional sports franchises across the NFL, NBA, MLB, and English Premier League remain family-controlled, according to Dakota’s Institutionalization of Sports report (June 2026). That's 96% of all franchises, despite five years of accelerating institutional capital flows into the asset class.

In this article, we'll discuss why family ownership has proven so structurally durable, what the rise of institutional capital actually looks like alongside it, and what generational transitions on the horizon could mean for the ownership mix over the next decade. By the end, you'll have a clear read on how these two ownership models coexist and where the balance is likely to shift.

The Numbers Behind Family Dominance

The degree of family control varies meaningfully by league. The NFL and NBA are both 100% family-controlled at the principal-owner level, with 32 and 30 teams respectively. MLB sits at 97% family-controlled across 30 teams. The EPL is the most institutionally open of the four, with 17 of 20 clubs (85%) still family-controlled.

Institutional capital is present alongside family ownership in 30 of those 112 franchises, representing 27% of the total. The NBA leads with 15 teams carrying some form of institutional stake (50%), followed by the EPL at 6 (30%), MLB at 8 (27%), and the NFL at 5 (16%). The critical distinction: institutional capital in almost every case sits in a minority position alongside a family principal owner, not in place of one.

Two Structural Reasons Families Remain in Control

Family ownership's persistence is not sentimental. It is structural, rooted in how each league governs ownership and how families have historically managed these assets.

1. Voting Architecture

Each league requires a designated principal owner with majority voting rights, irrespective of economic ownership. The NFL and MLB go further, requiring principal-owner approval by a 75% supermajority of existing owners. That threshold is explicitly hostile to dispersed institutional ownership and hospitable to concentrated family control.

Concentrated voting also lets owners derive non-financial returns, including civic prestige and family legacy, that justify the discounted-cash-flow premia at which franchises trade.

2. Estate Planning

Sports franchises have historically benefited from favorable estate-tax treatment of intangible-heavy private business interests.

That advantage has been a meaningful incentive for families to retain ownership across generations. The 2017 Tax Cuts and Jobs Act exemptions sunset at the end of 2025, which is one structural factor our report identifies as likely to drive accelerated NFL family transitions and PE minority sales over 2026-2028.

Family Ownership Is Not One Category

Family ownership spans a wide range of structures. The common thread across all of them is concentrated control rights vested in a kinship structure rather than dispersed among institutional investors.

At one end are century-old multi-generational dynasties: the McCaskeys (Bears, since 1921), the Maras (Giants, since 1925), the Rooneys (Steelers, since 1933), and the Fords (Lions, since 1964). At the other end are recently-formed co-owner couples and founder-patriarchs with succession plans still being mapped. The governance and succession complexity differs enormously across these structures, even though the ownership category label is the same.

The most consequential family owners have built cross-league portfolios that function like institutional platforms. The Kroenke/KSE group controls the Rams, Nuggets, Avalanche, Arsenal, and Colorado Rapids across NFL, NBA, NHL, EPL, and MLS, with an estimated combined value of approximately $21 billion. Mark Walter's Guggenheim group spans the Dodgers, Lakers, and Chelsea LP at approximately $20 billion. Josh Harris's HBSE controls the 76ers, Devils, Commanders, and Crystal Palace LP at approximately $15 billion. These are not passive family custodians. They are multi-sport capital allocators operating with the same consolidation logic as the institutional platforms now entering the market.

Dakota Marketplace tracks the institutional investment firms, family offices, and allocators actively evaluating sports vehicles. If you're raising a dedicated sports fund and want to identify which allocators have the mandate and the appetite, book a demo to see the full coverage.

The Institutional Capital That Has Arrived Is Additive, Not Replacing

The 30 franchises carrying institutional capital are not cases where families have exited. In almost every instance, a family or individual principal owner retains control, and institutional capital flows in alongside as a minority stake. The NFL's August 2024 framework codified this explicitly: approved private equity firms can hold up to 10% per team, with no economic voting rights, and the family principal owner retains full governance authority.

The one significant exception in our report is Chelsea FC, acquired by BlueCo in 2022 in a Clearlake Capital-led transaction at £4.25 billion. That represents the only majority-control transaction led by an institutional PE firm across the four leagues covered. Every other institutional position sits behind a family or individual at the governance level.

For fund managers raising sports vehicles, this distinction matters. The pitch to a family principal owner is not a buyout conversation. It is a liquidity and portfolio-diversification conversation, one that requires understanding what the family cares about beyond financial return.

The Generational Transition Pipeline

The next decade is likely to see meaningful ownership change, not because institutional capital is displacing families, but because several long-tenured NFL families face explicit succession decisions. The McCaskeys, Maras, Rooneys, and Fords collectively represent over a century of multi-generational NFL ownership. As those transitions play out, we expect them to be a primary catalyst for private equity minority sales rather than outright control changes.

The Seattle Seahawks sale, the $3.9 billion Padres control sale, and the Manchester City financial-charges verdict are identified in the report as the most consequential near-term catalysts. Combined with the estate-tax exemption sunset, these forces are likely to produce a more active transaction environment over 2026-2028 than the prior five years, even as institutional LPs backing sports GPs remain in minority positions by design.

The longer-term picture is one of coexistence. Families retain control. Institutional capital takes minority positions. The ownership mix shifts incrementally with each generational transition and each new PE-approved framework. The question for pension funds and other long-horizon allocators backing sports GPs is not whether families will be replaced, but how the minority-stake market deepens as more families choose institutional liquidity partners over the next decade.

Find Sports and Family Office Allocators on Dakota Marketplace

Dakota Marketplace tracks allocators actively investing in or evaluating alternative assets including dedicated sports vehicles. Filter by investor type, AUM tier, alternatives allocation, and prior commitment history. Book a demo to see the full coverage.