IN THIS REPORT

-

Market Overview - how $514.1B of franchise value is distributed across 112 teams in the four leagues we cover.

-

The Investment Case - returns, correlations, durable cash flows, and recession resilience - the LP case for sports as a strategic allocation.

-

League Profiles - ownership Characteristics and Competitive Dynamics Across Four of the World's Most Valuable Sports Leagues: The NFL, NBA, MLB, and EPL.

-

Three Drivers of Franchise Value - the forces compounding franchise value: media rights, scarcity, and global digital monetization.

-

Valuations & Sale Comparables - the world's $8B+ club, recent sale comparables, and franchises clearing 40%+ premia to Forbes valuations.

-

Family & Multi-Team Ownership - why families remain dominant and the cross-league empires consolidating ownership.

- Private Equity in Sports - the PE timeline since 2019, the NFL's August 2024 opening, and the most active firms.

- The Institutional Platforms - detailed profiles of the 16 firms shaping institutional capital flows into sports today.

- Funds in Market - the five funds currently raising and the seven GPs likely to return to market in the next 18-36 months.

- Investors Backing Sports GPs - the investor categories committing to sports vehicles: family offices, sovereigns, insurance, pensions, wealth platforms.

- Market Outlook - the pipeline, generational transitions, and the structural forces shaping the next decade.

EXECUTIVE SUMMARY

Professional sports franchises have evolved from passion-driven ownership assets into institutional-quality investments. Across the NFL, MLB, NBA, and English Premier League, franchise values now exceed $500 billion, driven by limited supply, accelerating media rights revenue, expanding global audiences, and the emergence of new institutional capital sources.

While family ownership remains the dominant model - roughly half of all franchises across the four leagues - the past five years have marked a shift toward institutional participation. The NFL's August 2024 decision to permit private equity investment represents a generational milestone, opening the most valuable sports league in the world to a new class of investors. KKR's February 2026 acquisition of Arctos Partners for $1.4 billion further validated professional sports as a core alternative asset class.

This report analyzes ownership structures, valuation trends, private equity penetration, and multi-team ownership dynamics across all 112 franchises. We find that continued institutionalization, evolving capital structures, and a coming wave of generational ownership transitions are likely to remain the primary drivers of franchise value creation across the global sports landscape over the next decade.

KEY TAKEAWAYS

1. Sports franchises have delivered strong long-term appreciation while maintaining a differentiated return profile from traditional and alternative asset classes.

The Ross-Arctos Sports Franchise Index (RASFI) generated 16.0% annualized returns over the trailing 10 years through 01 2026. Historical analyses suggest sports franchise valuations have exhibited low correlation with equities, fixed income, private equity, private credit, real estate, and infrastructure, making the asset class a compelling diversifier within long-duration portfolios.

2. The NFL's August 2024 PE opening is the most notable shift in a decade.

Only seven approved firms, a 10% per-team cap, and a 75% owner-approval threshold. Multiple deals have closed in the first 18 months (Bills/ Arctos, Dolphins/ Ares, Chargers/ Arctos, Browns/ Arctos, Patriots/Sixth Street); we expect 8-12 more over the next 18 months as approved firms deploy initial allocations.

3. KKR's $1.4B February 2026 acquisition of Arctos is the clearest validation yet that sports is a core alternative asset class.

Arctos holds positions in 15 of the institutional sports franchises in our coverage, roughly half the institutional market. KKR's perpetual-and-long-dated capital base (now 53% of $759B AUM post-Arctos) is purpose-built to hold sports minority positions across the multi-decade hold periods league rules effectively require.

4. Sports fundraising has reached considerable breadth, with nine active fundraises currently in market and a growing pipeline of recently closed managers likely to return over the next several years.

LPs can now access strategies spanning franchise ownership, sports credit, media finance, operating companies, women's sports, and sports technology through both institutional-scale platforms (Arctos, Apollo, Ares, TPG) and specialist managers (Monarch, Otro, Harbinger, Sportsology, and others). The available opportunity set is broader than at any prior point in the asset class's evolution.

MARKET OVERVIEW

The NFL, MLB, NBA, and English Premier League collectively represent approximately $514.1 billion in franchise value across 112 teams, making professional sports one of the largest and most valuable segments of the global alternatives universe. The market is highly concentrated: the 32 NFL teams alone account for $227 billion - 44% of combined value across the four leagues despite representing only 29% of team count.

Sports franchises occupy a distinctive position in the institutional alternatives landscape. Unlike most private investments, they combine fixed and league-protected supply with broadly distributed, contractually predictable revenue (national media rights, salary cap mechanics, revenue sharing). This combination produces three uncommon characteristics simultaneously: scarcity, low cash-flow volatility, and an emotional ownership premium. Few asset classes share all three - real estate has scarcity but cash-flow volatility, venture has volatility without scarcity, treasuries have neither. Sports franchises function more like an indexed scarcity instrument with operating leverage to media and live events economics.

LEAGUE SNAPSHOT

THE INVESTMENT CASE

THE INVESTMENT CASE

For institutional allocators evaluating sports as a discrete asset class, four characteristics differentiate it from the broader private-markets opportunity set.

- Scarcity-Driven Asset Appreciation

The combination of limited franchise supply, contractual revenue streams, and increasing global demand for live sports has supported decades of franchise value growth. Through 01 2026, RASFI delivered 16.0% annualized returns over the trailing 10 years and 13.1% annualized returns over the trailing 20 years.

- Low Correlation to Public Equities and Most Private Alternatives

Sports franchise returns are primarily driven by factors such as media and commercial revenue growth, live-event demand, fan engagement, league economics, and the limited supply of franchise ownership opportunities. These drivers are generally distinct from the factors that influence public equities, fixed income, and many other private market investments. Consequently, sports franchises have historically exhibited relatively low correlation with traditional asset classes, making them a potentially valuable source of diversification within long-term investment portfolios.

- Contractually Durable Cash Flows Backed by Long-Dated Media Rights

League-wide media rights are negotiated centrally, revenue-shared, and locked in for 10-11 year terms. The NFL's $113B media package runs through 2033; the NBA's $76B renewal runs through the 2035-36 season. Eighty of the top 100 US broadcasts in 2024 were sporting events - a key advantage in the streaming era - and combined with multi-year sponsorship contracts and recurring stadium revenue, the asset compounds with league revenue rather than management quality.

- Lower Realized Volatility and Demonstrated Recession Resilience

Franchises rarely transact, and sale prices have risen monotonically for over a decade, yielding a return series with low realized variance. CAIS analysis indicates sports franchise returns have outperformed traditional and alternative asset classes during downturns; Ross-Arctos data spanning 2008-2024 shows positive long-term returns at lower risk than equities, PE, private debt, real estate, and infrastructure.

The principal trade-off is illiquidity- six-year minimum hold periods under NFL rules and similar restrictions across other leagues, no economic voting rights for institutional minority investors, and a thin secondary market. For LPs with long horizons and a need for diversification beyond traditional alternatives, sports increasingly fits the profile of a strategic allocation rather than a niche curiosity.

LEAGUE PROFILES AT A GLANCE

The four leagues differ materially in ownership character and PE openness. The NFL is the most valuable and most family-entrenched: 32 teams aggregating $227.4B, predominantly family-controlled, and the strictest PE framework (7 approved firms, 10% per-team cap, sovereign-wealth excluded). The NBA, at 30 teams and $160.?B, leads the four leagues in valuation growth (17.2% 10-year CAGR), driven by its $76B media-rights renewal and global expansion; one-third of NBA teams now carry an institutional PE stake. MLB ($87.2B across 30 teams) has the most permissive US framework- 30% per-team cap and the longest PE track record (Arctos approved 2019) - but lags on growth (8.4% CAGR) as RSN economics restructure. The English Premier League ($39.2B across 20 clubs) is the most globally diverse, the only league with majority-PE control (Clearlake / Chelsea), and the least regulated on cross-border and sovereign capital.

THREE DRIVERS OF FRANCHISE VALUE

-

Media Rights Inflation. League-level broadcast deals are the single largest revenue driver. The NFL's current media package (Amazon, Apple, ESPN, NBC, CBS, Fox, Disney, YouTube) is worth approximately $113B over 11 years; the NBA's 2024 renewal with ABC/ESPN, NBC/Peacock, and Amazon Prime is worth $76B over 11 years. These rights are sold league-wide and revenue-shared, dampening downside risk and driving uniform appreciation across each league.

-

Scarcity. The NFL has not added a team since the Houston Texans began play in 2002. MLB last expanded with the Diamondbacks and Rays in 1998. The NBA has been at 30 teams since 2004. The EPL operates with promotion relegation but has been held at 20 clubs since 1995. With a fixed supply of franchises and growing demand, the price discovery dynamic is biased upward.

-

Global Audience Expansion & Digital Monetization. Sports content is the only mass-audience programming consistently watched live in the streaming era - 80 of the top 100 US broadcasts in 2024 were sporting events. League-level international expansion (NBA in China and India, NFL in UK/Germany/Mexico, EPL globally) creates additional fan-revenue tailwinds, and the shift from cable to streaming has broadened the bidder universe (Amazon, Apple, Netflix, Disney, NBC/Peacock, YouTube), lifting media rights pricing. Digital revenue diversification - fan data, direct-to-consumer products, sports betting, social and creator activations - is now a meaningful and growing component of franchise economics.

WHY SOME LEAGUES OUTSPACE OTHERS

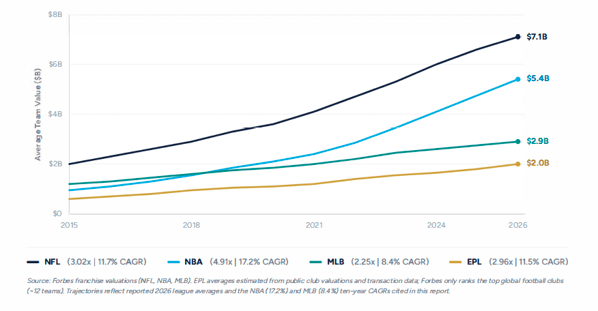

The NFL leads on absolute value and consistency - the largest media package by far ($1138 over 11 years), the deepest US fan base, and the strictest supply constraint (32 teams since 2002). The NBA leads on growth - international expansion, younger demographics, social-media engagement, and a $768 media-rights step-up beginning the 2025-26 season.

MLB has lagged primarily because of regional sports network (RSN) economics restructuring - the 2023 Diamond Sports/ Bally Sports bankruptcy disrupted the local-market media model MLB disproportionately depends on. The EPL's average lags because it spans 20 clubs with wide dispersion: top clubs (Manchester United, Liverpool, Arsenal, Chelsea, Manchester City) command $3-68+ valuations while bottom-half clubs trade at fractions of US averages.

LEAGUE AVERAGE TEAM VALUE, 2015 - 2016

TOP 10 MOST VALUABLE SPORTS FRANCHISE

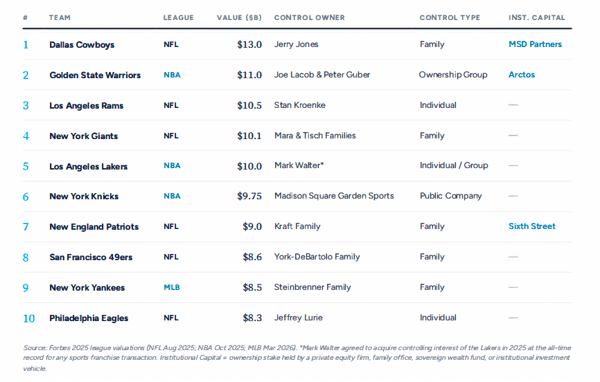

The world's ten most valuable sports franchises all sit comfortably above $88 and are exclusively US-based - no Premier League club appears in the global top fifteen, with Manchester United at $6.68 ranking approximately 18th by enterprise value. Five of the ten are family-controlled; the remaining structures span individual principal owners, ownership groups, and one publicly traded entity (Madison Square Garden Sports/ Knicks). Three of the ten now carry institutional capital - Arctos at the Warriors, Sixth Street at the Patriots, and MSD Partners at the Cowboys.

Several patterns stand out. The NFL holds 6 of the top 10 spots, the NBA 3, and MLB 1 (Yankees)-no Premier League club makes the global list, with Manchester United at $6.60B ranking approximately 18th. Five of the ten franchises are pure family-controlled; the remaining structures are more varied, including two individual owners (Kroenke/ Rams, Lurie/ Eagles), one ownership group (Lacob / Guber at the Warriors), a hybrid individual/ ownership group (Walter at the Lakers post-2025 sale), and one publicly traded entity (Madison Square Garden Sports/ Knicks). Three of the top ten carry institutional capital -Arctos at the Warriors ( ~13%), Sixth Street at the Patriots (~3%), and MSD Partners at the Cowboys. The Walton-Kroenke extended family commands particular scale, controlling two of the top 10 directly (the Rams at #3 plus indirect involvement in the Broncos via the separately-held Walton-Penner Group).

RECENT FRANCHISE SALE COMPARABLES

Franchise sale prices over the past seven years tell a clear story: the sale-comp ceiling has more than quadrupled, from $2.3B in 2018 (Panthers/ Tepper) to $10.0B in 2025 (Lakers / Walter). Six of the eight largest sports franchise sales in history have closed since 2022, and every league we cover has set a new control-sale record within the past four years. Recent benchmarks: Lakers $10.0B (2025), Celtics $6.18 (2025), Commanders $6.05B (2023), Broncos $4.65B (2022), Chelsea $4.25B (2022), Suns $4.0B (2023).

Sales are clearing at meaningful premia to Forbes valuations (Lakers ~40%, Celtics ~30%, Commanders ~8%), and only one of these listed control sales (Chelsea/ BlueCo, 2022) was led by an institutional PE firm - the prevailing model remains family-led majority ownership with institutional capital flowing in alongside rather than replacing it.

Family Ownership Analysis

Family ownership remains the dominant ownership structure across the four leagues covered in this report (roughly half of all teams). It is not a uniform category - spanning century-old multi-generational dynasties, founder-patriarchs with succession plans, and recently-formed co-owner couples - but the common thread is concentrated control rights vested in a kinship structure rather than dispersed among institutional investors.

WHY FAMILIES DOMINATE

Family ownership remains the leading structure across these leagues (roughly half of all teams across the four leagues) for two key reasons. First, each league requires a designated principal owner with majority voting rights irrespective of economic ownership, and the NFL and MLB require principal-owner approval by 75% supermajority- hostile to dispersed ownership and hospitable to family control. Concentrated voting also lets owners derive non-financial returns (civic prestige, family legacy) that justify the discounted-cash-flow premia at which franchises trade. Second, sports franchises have historically benefited from favorable estate-tax treatment of intangible-heavy private business interests; the 2017 Tax Cuts and Jobs Act exemptions sunset at the end of 2025, which is one factor we expect to drive accelerated NFL family transitions and PE minority sales over 2026-2028.

MULTI-TEAM OWNERSHIP EMPIRES

A small number of ownership groups now control assets across multiple leagues, compounding brand, media, and real-estate value. These cross-league portfolios are the family-side equivalent of the institutional platforms covered in the next section - same consolidation logic, different actor type.

PRIVATE EQUITY IN SPORTS OWNERSHIP

PRIVATE EQUITY IN SPORTS OWNERSHIP

Institutional capital has become a meaningful and growing source of equity for major league franchises. Across the four leagues we cover, 30 of 112 franchises (27%) now carry some form of institutional capital on the cap table - private equity funds, family offices, sovereign wealth funds, or PE/HF founders investing via personal-wealth vehicles. The pace accelerated after MLB became the first major US league to formally approve an institutional minority investor (Arctos) in 2019, and again after the NF L's August 2024 PE opening.

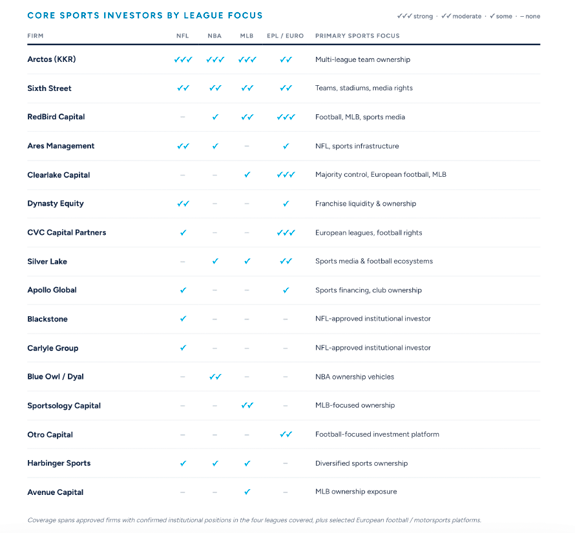

MOST ACTIVE INSTITUTIONAL PE FIRMS

THE INSTITUTIONAL PLATFORMS

PLATFORM PROFILES

Arctos Partners

Arctos closed Sports Partners Fund II at $4.1B in 2024 and is the only firm approved by all five US leagues (NFL, NBA, MLB, NHL, MLS) plus global motorsports and European soccer. Beyond 14 US team positions it holds equity in Liverpool, Paris Saint-Germain and Aston Martin F1, and launched Arctos Capital Markets in September 2024 as the first wealth-channel sports product. KKR acquired Arctos in February 2026 for $1.4B + $550M earn-out, folding the platform into a new KKR Solutions unit backed by KKR's $759B AUM distribution machine.

Sixth Street Partners

Sixth Street has built the most diversified mid-tier platform: NFL (Patriots ~3%), NBA (Spurs ~20%, Celtics ~12.5%), and MLB (SF Giants), plus stadium and media-rights finance with Real Madrid (€360M Bernabeu) and FC Barcelona (€517.SM for 25% of LaLiga TV income). It is also lead investor in the Bay Area NWSL expansion franchise - one of the few institutional players with meaningful women's-sports exposure.

RedBird Capital

RedBird is the most vertically integrated operator in the category, with a portfolio spanning European football (AC Milan, Liverpool via FSG, Toulouse), Formula 1 (Alpine), media and distribution (YES Network, EverPass with the NFL, lead role in the $8.4B Skydance-Paramount merger), college sports (College Athlete Solutions), and emerging sports (MARI tennis with Apollo, UFL spring football). The model is teams+ media + distribution under one roof - closer to a vertically integrated sports holding company than a traditional PE fund.

Ares Management

Ares raised a $3.?B dedicated Sports/ Media/ Entertainment fund in 2022 and built a cross-sport portfolio: NFL (Miami Dolphins ~10%, December 2024), European football (Chelsea LP, Olympique Lyonnais, Inter Miami MLS, Atletico Madrid), and Formula 1 (McLaren Racing). The Dolphins deal was one of the two first PE-NFL transactions to close, and the dedicated fund vehicle was a template several other firms have since followed.

Clearlake Capital

Clearlake Capital (~$90B AUM) anchors the most consequential majoritycontrol sports transaction in recent history: the 2022 BlueCo / Boehly acquisition of Chelsea FC for £4.25B / $4.25B. The firm also holds Strasbourg through BlueCo, is leading the proposed $3.9B Padres control sale (pending MLB approval), and co-backs MARI tennis with Apollo and Red Bird - distinguished from peers by emphasis on majority control rather than minority stakes.

Dynasty Equity

Dynasty Equity (~$343M AUM, founded 2022) is co-founded by Providence Equity's Jonathan Nelson and K. Don Cornwell, former Morgan Stanley global head of sports M&A. Cornwell's 30-year history advising NFL family owners (Bills, Steelers) earned Dynasty one of the seven NFL approved-firm slots; existing positions include a strategic minority in Liverpool FC (via FSG, $100-200M, 2023) and equity in TMRW Sports

(TGL golf league).

CVC Capital Partners

CVC Capital Partners brings the deepest pre-2024 European sports portfolio of any NFL-approved firm - long-term shares of LaLiga and Ligue 1 media income, Six Nations Rugby, the WTA, and prior Formula 1 ownership (2006-2017). CVC participates in the NFL-approved consortium with Blackstone, Carlyle, Dynasty Equity, and Ludis.

Silver Lake

Silver Lake (~$110B AUM) was an early mover into sports as an institutional category. Holdings include a ~10% stake in City Football Group (Manchester City+ global affiliates), an 8.6% position in New Zealand's All Blacks ($133.6M), Madison Square Garden Sports (Knicks + Rangers), Endeavor (UFC parent), Oak View Group, Diamond Baseball Holdings, and a $320M stake in Fanatics - emphasis on sports media, distribution, and football ecosystems rather than US-league franchisestakes.

FUNDS IN MARKET

The fund raising landscape for sports is the deepest it has ever been. For LPs evaluating commitments, the active opportunity set now spans a diverse set of institutional and specialist managers pursuing strategies across franchise ownership, sports credit, media finance, operating companies, and women's sports. Based on the funds currently in market and recent closes shown below, the market can be viewed in two cohorts: nine active fundraises currently in market and five recently closed platforms that could return to market over the coming fund cycles.

CURRENTLY IN MARKET

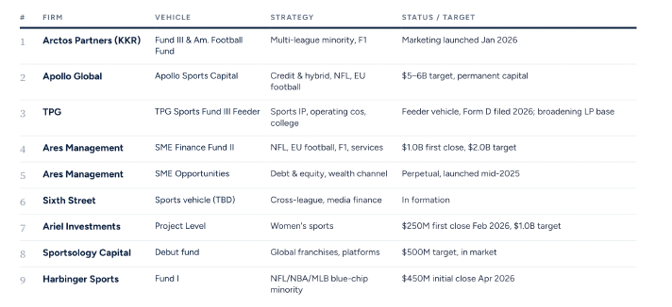

The current fundraising pipeline includes a mix of established institutional managers and emerging specialist sports investors. The largest vehicle is Apollo Sports Capital, targeting $5-6 billion through a permanent-capital structure focused on sports credit and hybrid financing opportunities. Other large-scale offerings include Ares Management's Sports, Media & Entertainment Finance Fund 11, targeting $2.0 billion, and Arctos Partners Fund Ill and American Football Fund, which continues Arctos' strategy of acquiring minority stakes across major sports leagues and Formula 1.

Beyond the flagship platforms, several specialist managers are raising capital around differentiated themes. TPG Sports Fund I is focused on sports intellectual property, operating companies, and college athletics. Sixth Street is reportedly developing a dedicated sports vehicle centered on cross-league opportunities and media finance. Ariel Investments' Project Level targets women's sports, while Sportsology Capital is raising a debut fund focused on global franchises and sports platforms. Harbinger Sports Fund I is pursuing minority investments in blue-chip NFL, NBA, and MLB franchises, and Ares SME Opportunities provides a perpetual vehicle investing across sports-related debt and equity opportunities.

Collectively, these vehicles represent the broadest set of institutional sports fundraising opportunities the asset class has seen, spanning ownership, financing, media, operating businesses, and adjacent ecosystem investments.

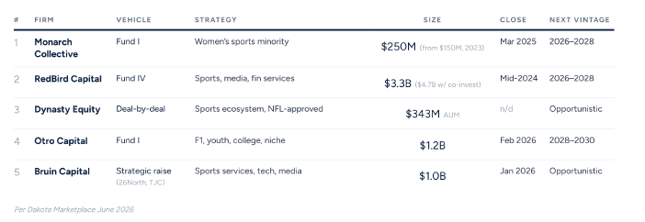

FUNDS ANTICIPATED BACK IN MARKET

A second cohort consists of managers that have recently closed funds and are expected to return to market during the next fundraising cycle. While precise timing will depend on deployment pace and market conditions, these platforms provide a view into the next generation of sports- focused opportunities.

Monarch Collective Fund I closed at $250 million in March 2025 and is focused on women's sports ownership and related opportunities. Red Bird Capital Fund IV, one of the largest dedicated sports investors globally, closed at approximately $3.3 billion and is expected to remain active across sports, media, and financial services. Otro Capital Fund I closed at $1.2 billion and focuses on Formula 1, youth sports, college athletics, and niche sports properties. Bruin Capital's strategic raise provides exposure to sports services, technology, and media businesses, while Dynasty Equity continues to pursue an opportunistic, deal-by-deal approach across the broader sports ecosystem.

Allocators building mature sports programs increasingly construct portfolios across multiple strategy types rather than concentrating solely on franchise ownership funds. Larger institutional platforms such as Arctos, Apollo, Ares, and TPG provide diversified exposure across leagues, financing structures, and sports-adjacent businesses. Specialist managers such as Ariel Investments (Project Level), Monarch Collective, Otro Capital, Sportsology Capital, and Harbinger Sports offer targeted access to themes including women's sports, Formula 1, college athletics, sports technology, and franchise-focused investing.

The combination of large-scale institutional managers and specialized sector investors creates one of the deepest opportunity sets the sports asset class has offered to LPs, with meaningful diversification available across leagues, capital structures, geographies, and underlying sports-related business models

INVESTORS BACKING SPORTS GPs

The investor base committing to sports vehicles is more diverse than most alternative asset classes, reflecting the long-duration nature of the assets, their cultural appeal, and the variety of access points now available. Six investor categories are actively deploying capital into institutional sports today.

1. Family Offices & UHNW

The dominant source of direct sports ownership capital. Multigenerational family offices, founders, and ultra-high-net-worth individuals continue to anchor most control transactions and remain important investors in dedicated sports funds. Recent examples include the Walton-Penner ownership group at the Denver Broncos (NFL), Mark Walter's investments in the Los Angeles Dodgers (MLB) and Los Angeles Lakers (NBA), Steve Cohen's acquisition of the New York Mets (MLB), and Julia Koch's minority investment in the New York Giants (NFL).

2. Sovereign Wealth Funds

Foreign sovereign capital remains concentrated in global football, particularly the Premier League, where ownership rules permit controlling foreign investors. Saudi Arabia's PIF controls Newcastle United, while Abu Dhabi-backed ownership controls Manchester City. Sovereign participation has been far less prevalent in North American sports; notably, the NFL excluded sovereign wealth funds from its 2024 institutional ownership framework.

3. Pensions & Endowments

Slow but accelerating institutional adoption. Public pension funds, university endowments, retirement systems, and foundations are increasingly evaluating dedicated sports investment strategies. Institutional investors were important participants in Otro Capital's $1.2 billion Fund I-one of the largest first-time sports-focused funds raised globally. While allocations remain modest relative to buyout, infrastructure, private credit, and real estate strategies, institutional interest has increased as the sports asset class has developed a longer published performance record and a growing set of dedicated investment vehicles.

4. Insurance Balance Sheets

Insurance-affiliated capital pools are becoming an increasingly important source of institutional capital for sports. Platforms such as Apollo's Athene and KKR's Global Atlantic provide access to longduration liabilities that align naturally with sports assets' multi-decade holding periods. KKR's February 2026 acquisition of Arctos was explicitly framed as expanding the firm's perpetual and long-dated capital base, which would represent 53% of KKR's $759 billion AUM post-transaction. Apollo's permanent-capital structure for Apollo Sports Capital reflects a similar emphasis on patient, long-duration capital.

5. Private Wealth Platforms

The newest and potentially largest future LP channel. Arctos Capital Markets is the first dedicated sports ownership capital-markets platform launched by a major institutional sports investor, connecting qualified wealth-channel investors with direct franchise ownership opportunities. iCapital and CAIS - the two largest US alternative investment marketplaces - now distribute sports vehicles to financial advisors and family offices.

6. Athletes & Operators

A growing but specialized category. Active and retired athletes participate via direct minority team positions and athlete-advisor structures - Mark Cuban at the Mavericks (NBA), Joe Tsai at the Nets (NBA) and the Dolphins (NFL), Patrick Mahomes at the Royals (MLB), and LeBron James at Liverpool (EPL, via Fenway Sports Group) among the most prominent. The economic stake is typically modest relative to the institutional LPs above; the value is sourcing, brand association, and operating insight.

LP appetite for sports has broadened over the past five years. The convergence of insurance balance sheets seeking long-duration assets, wealth platforms seeking differentiated alternatives, family offices seeking trophy-with-yield, and athletes seeking equity in their industry has created a deeper and more durable demand pool than the sports investment landscape has ever had.

MARKET OUTLOOK

The pipeline for sports franchise transactions is deep and well supported. The NFL's August 2024 opening to institutional capital - only seven approved firms with a 10% perteam cap - has created a dynamic where institutional demand far exceeds available supply, and we expect 8 to 12 additional NFL minority-stake transactions over the next 18 months as approved firms deploy initial allocations. The NBA's $76B media-rights renewal began with the 2025-26 season; the multi-year valuation step-up has yet to fully arrive in Forbes valuations and is likely to drive a further leg of franchise appreciation, particularly in mid- and small-market teams.

Generationally, several long-tenured NFL families face explicit succession decisions in the next decade - the Mccaskey (Bears, since 1921), Mara (Giants, 1925), Rooney (Steelers, 1933), and Ford (Lions, 1964) families. The 2017 Tax Cuts and Jobs Act estate-tax exemptions sunset at the end of 2025, which we expect to drive accelerated NFL family transitions and PE minority sales over 2026-2028. The Seattle Seahawks sale, the $3.9B Padres control sale, and the Manchester City financial charges verdict are the most consequential near-term catalysts.

The longer-term growth story is the wealth channel. Franchise interests are cash-generative, long-duration, and naturally suited to evergreen and semi-liquid vehicles - the format that accelerated adoption of private credit and real estate. The KKRArctos combination is the clearest signal yet that the biggest alternative asset managers now view sports as a core distribution category. The principal risk: as more capital chases a fixed pool of franchise interests, entry multiples are rising - platforms that bring distribution, co-investment, and media rights expertise will win the best deals.

ABOUT THIS REPORT

This report was built entirely on data from Dakota Marketplace - the most comprehensive private markets database designed fro the institutional investment community. Every team valuation, ownership structure, transaction figure, family-tenure record, and private equity investment referenced in these pages was researched and verified by Dakota's 60-plus person data team.

DAKOTA MARKETPLACE

A database of LPs, GPs, private companies, and public companies used by fundraising and deal-sourcing teams to both raise capital and source investment opportunities. Over 1,300 global investment firms use Dakota daily.

For further insights, book a demo.