*Form D Filing count is focused on pooled investment vehicles only. This analysis includes only new notices, not amendments to previous filings

**This figure reflects the aggregate dollars reported in the “total amount sold” field.

***Dollar figure includes commitments that were disclosed and tracked in February (not necessarily when the commitment officially took place)

Private Equity

Private equity fundraising continues to be driven by the largest managers. Most new launches are large flagship or adjacent strategies with multi-billion dollar targets. Blackstone is preparing a first close for Energy Transition Partners V that should exceed the $5.6 billion raised by its predecessor and is also nearing a major close for Strategic Partners X, targeting at least the $22 billion raised for its last secondaries flagship. CVC is pre-marketing Fund X after raising €26 billion previously, and Petershill is reportedly targeting $5 billion for its next GP stakes fund. Managers are also leaning into focused themes. Apollo Sports Capital plans to deploy roughly $5 to $6 billion, Ares is launching a European sports, media, and entertainment strategy, Blue Owl has raised more than $3 billion for a new strategic equity and secondaries vehicle, and HarbourVest closed a continuation fund of more than $1.1 billion.

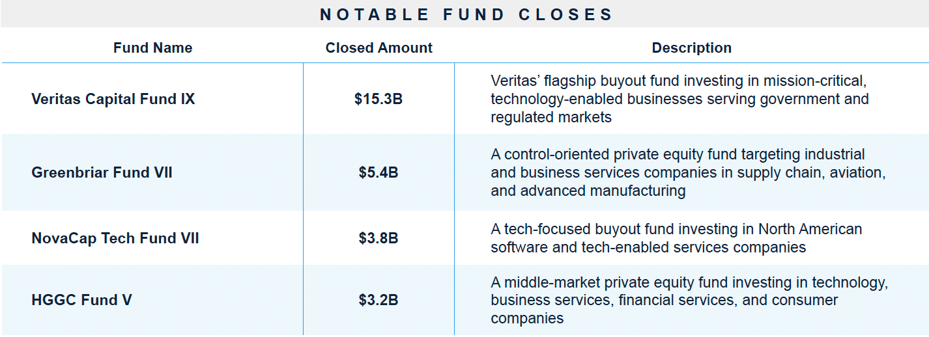

Successor closes have reinforced the momentum. Veritas Capital raised $15.3 billion for Fund IX, HGGC closed Fund V at $3.2 billion, Novacap’s Technologies Fund VII reached nearly $3.8 billion, and JLL Partners raised $1.4 billion for Fund IX. In the middle market, firms such as Union Capital ($450 million), Bestige ($240 million), and Dynamic Core ($240 million) exceeded targets, while emerging managers brought debut funds to market in the $75 million to $600 million range. Climate and impact vehicles are also advancing, including DPI’s African Development Partners IV targeting $1 billion and GEF’s South Asia Growth Fund IV seeking up to $600 million.

Private Credit

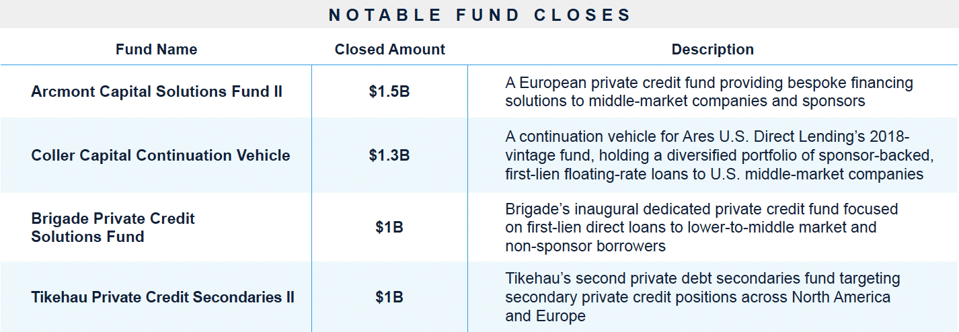

On the private credit front, Ares, which raised $113 billion in 2025, is preparing to launch its fourth U.S. senior direct lending fund, with a potential first close in Q4 2026, and its seventh European direct lending fund. It is also closing a commingled alternative credit vehicle expected to match the $6.6 billion raised by its predecessor. Capza marked a €1.4 billion first close toward a roughly €3 billion target for Capza Private Debt 7, Tikehau raised more than $1 billion for its second private debt secondaries strategy, Brigade closed its first private credit fund at over $1 billion, and Arcmont Capital Solutions II reached €1.5 billion, nearly double the size of its prior fund.

Specialized strategies are moving forward alongside the larger direct lending platforms. Viola Credit launched a $300 million Customer Growth Financing fund focused on fintech and AI-driven companies. Infrastructure debt is gaining traction, with Allianz raising just over €1 billion for their Infrastructure Credit Opportunities Fund II and ETIC targeting €150 million for a renewable energy debt vehicle. Structured and rated credit products are getting attention as well, including GCM Grosvenor’s $625 million structured alternatives strategy and a $250 million asset-backed credit interval fund launched by Privacore and Victory Park.

Real Assets

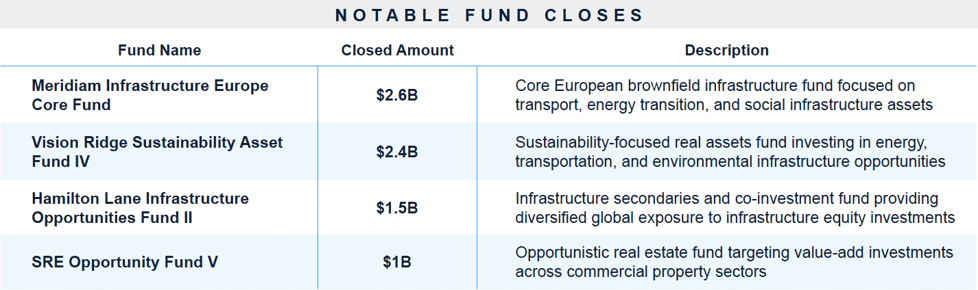

Real assets fundraising from February concentrated in infrastructure, climate transition, and sustainable real estate, with several vehicles targeting or exceeding $1 billion. Vision Ridge closed Sustainable Asset Fund IV at $2.4 billion, nearly double the size of its prior fund, and Meridiam completed a €2.2 billion Europe-focused infrastructure continuation fund. Hamilton Lane’s Infrastructure Opportunities Fund II raised $1.5 billion, plus nearly $400 million in related vehicles, and Kinterra closed its critical materials fund at a $950 million hard cap. Eversource Capital has reportedly begun marketing a $700 million green infrastructure fund focused on India and South Asia, while Patrizia and Mitsui launched an Emerging Asia Sustainable Infrastructure Fund targeting $300 million, with a $500 million hard cap.

In real estate, managers launched a mix of traditional closed-end funds and larger, more flexible vehicles. Hongkong Land introduced the Singapore Central Private Real Estate Fund with SGD 8.2 billion in AUM and SGD 4.1 billion in committed equity. Covenant Capital raised $860 million for an apartment fund along with $269 million for an affordable housing sidecar. Thompson Thrift secured $222 million for multifamily development, and Azora’s Southern European Opportunities III surpassed €840 million and could reach up to €1.4 billion.

Venture Capital

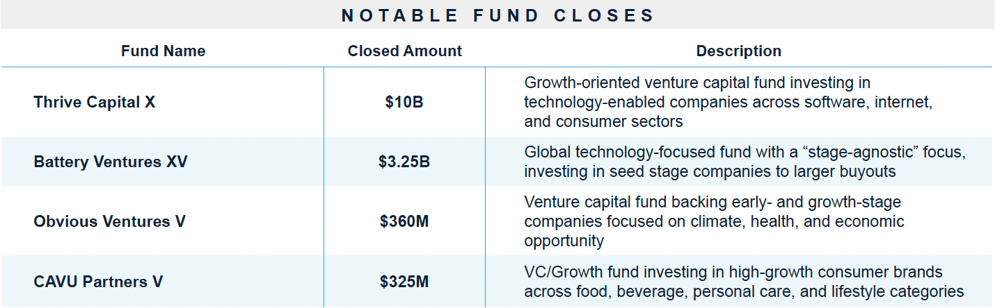

At the large end, several VC managers closed or are raising large flagship vehicles last month. Thrive Capital reportedly closed Fund X at more than $10 billion, and Battery Ventures XV raised $3.25 billion. Mundi Ventures secured a €750 million first close toward a €1.25 billion target, and Layer Global is targeting $1.1 billion for an early-stage technology fund. In growth and late-stage strategies, Artemis Ventures is targeting JPY 50 billion, or roughly $319 million, for Japanese startups, and Square Peg Capital raised $650 million across two vehicles. The larger raises point to renewed conviction in areas such as AI infrastructure and enterprise software.

Smaller VC managers were also able to raise significant capital. Primary Venture Partners is deploying $625 million into AI startups, while Elaia launched its fifth digital fund with a €120 million first close. Defense and space strategies are gaining traction, including Seraphim’s space fund surpassing $100 million and Masna Ventures targeting more than $100 million for defense tech. Global funds had success bringing in capital as well, with Peak XV raising $1.3 billion across India and APAC vehicles and several India-focused funds closing between $50 million and $150 million.

Key Takeaways

Large Managers Succeed in Fundraising

The largest managers continue to lead the market. Firms like CVC and Blackstone are preparing major vehicles across buyout, secondaries, and infrastructure. Established managers with strong track records and global LP relationships are capturing a significant share of assets raised.

Secondaries Becoming Commonplace Across Strategies

Secondaries are now a standard part of the market, and not just limited to private equity. Coller Capital completed a $1.3B continuation vehicle for Ares’ direct lending platform, Ardian has already raised $5.2B for its infrastructure secondaries fund, and Tikehau closed their second debt secondaries fund. The strategy is now widely used across multiple asset classes.

Sustainable Infrastructure in Focus

Capital continues to flow into sustainable and energy transition strategies. Vision Ridge closed its Sustainable Asset Fund IV at $2.4B, Meridiam raised €2.2B for a Europe-focused infrastructure continuation fund, and Kinterra hit a $950M hard cap for its critical materials fund. Energy transition, renewables, and decarbonization remain key areas of interest for institutional investors.

Venture Capital Gaining Traction

Venture fundraising picked up, especially among larger and technology-focused firms. Thrive Capital raised $10B, Battery Ventures closed $3.25B, and Peak XV secured $1.3B across India and APAC vehicles. There is strong interest in artificial intelligence, defense technology, and deep tech, with funds like Seraphim’s space strategy surpassing $100M.

About Dakota

Dakota is a financial, software, data and media company based in Philadelphia, PA. Dakota’s flagship product, Dakota Marketplace, is a database of LPs, GPs, Private Companies and Public Companies used by thousands of fundraising, deal, and investment teams worldwide to raise capital, source deals, track peers, and access comprehensive data—all in one global platform. For more information, book a demo of Dakota Marketplace!