*Form D Filing count is focused on pooled investment vehicles only. This analysis includes only new notices, not amendments to previous filings

**This figure reflects the aggregate dollars reported in the “total amount sold” field.

***Dollar figure includes commitments that were disclosed and tracked in January (not necessarily when the commitment officially took place)

Fundraising Highlights

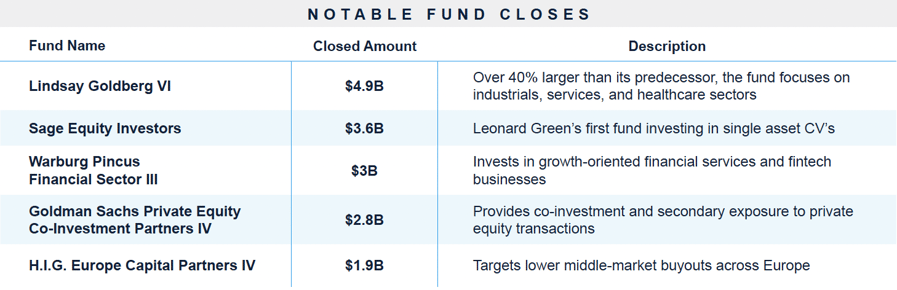

Private Equity

In private equity, Clayton, Dubilier & Rice has entered early discussions for its next flagship vehicle, Fund XIII, which is targeting $26 billion and could reach more than $28 billion including GP commitments. A formal launch is expected in the first half of 2026. If successful, the fund would rank among the largest raised to date and continue CD&R’s long-standing focus on control investments in large North American and European businesses across healthcare, consumer and retail, technology, industrials, and business services. Francisco Partners is pursuing a similar path, setting a $14 billion target for its eighth flagship buyout fund and already securing commitments from several major public pensions. The fund will invest alongside Francisco Partners Agility IV, which is targeting $4 billion.

Beyond traditional buyouts, specialized strategies are gaining traction. Arctos Sports Partners has filed for its third flagship fund following the $4.1 billion close of Fund II in 2024, extending its strategy of acquiring minority stakes in professional sports franchises and providing liquidity solutions to team owners. Warburg Pincus, meanwhile, is reportedly exploring a Europe-focused defense fund targeting €1 billion to €1.5 billion, aimed at capturing increased defense spending and investment in regional security amid heightened geopolitical uncertainty. In GP-led secondaries, Parthenon Capital Partners is testing investor appetite for a continuation vehicle of up to $1.7 billion to extend ownership of Kroll Bond Rating Agency.

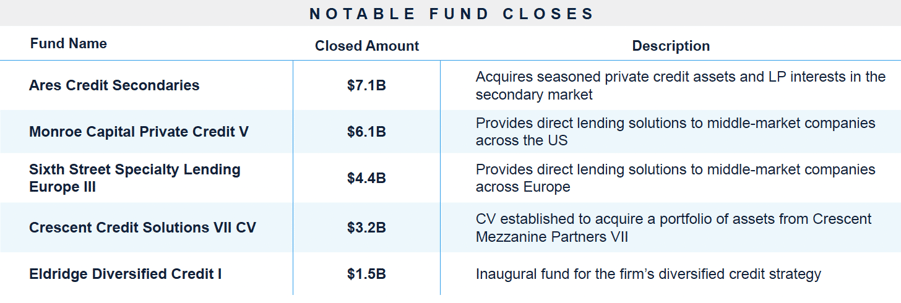

Private Credit

On the private credit front, Alcentra is targeting €600 million for the third vintage of its European special situations strategy, focused on stressed, distressed, and event-driven opportunities that offer diversification in volatile markets. Invesco has launched an open-ended European Upper Middle Market Income Fund under the revised ELTIF 2.0 framework, targeting senior secured lending and illustrating how managers are increasingly using evergreen and semi-liquid structures to access retail and wealth capital. PGIM is also expanding its platform with plans to deploy $1 billion over two years through a dedicated private credit secondaries strategy in the U.S. and Europe, reflecting the convergence of strong secondaries demand and continued growth in private credit allocations.

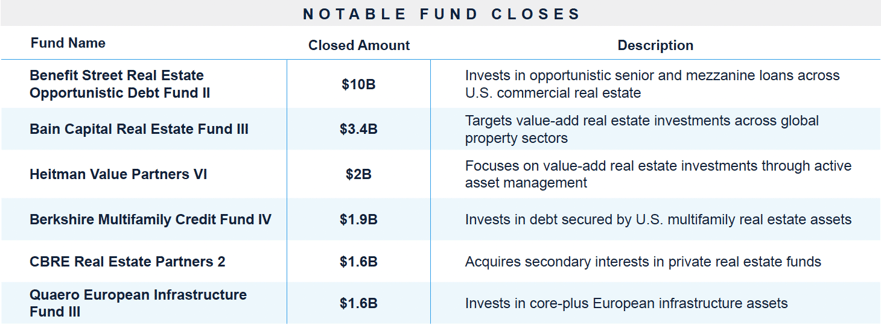

Real Assets

Real Assets was one of the more active areas within the market with a number of notable large franchises wrapping up fundraising and new funds launched. Goldman Sachs began to market a Japan-focused real estate fund targeting $500 million, with an emphasis on data centers, logistics, residential, and hospitality assets and mid-teens return targets. ActivumSG has begun marketing its first sector-specific vehicle, a hospitality-focused fund targeting nearly $300 million for investments across Southern Europe, particularly Spain and Portugal. Tortoise Capital Advisors, subject to regulatory approval, plans to launch an energy and infrastructure interval fund in the second half of 2026, offering blended exposure to public and private assets across energy, midstream, power, utilities, and adjacent infrastructure. StepStone Group has also expanded its real estate platform with the launch of S-Core, a lower-risk core and core-plus offering focused on secondaries, co-investments, and targeted operating company investments.

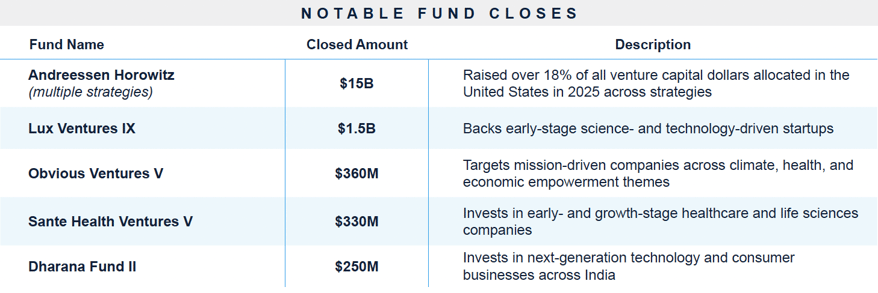

Venture Capital

In venture capital, Battery Ventures is targeting $3.2 billion for its 15th flagship fund, with commitments already secured from global institutions, and will invest across early-stage, growth, and buyout opportunities in North America, Europe, and Israel. In Europe, Nextgen Ventures has launched its third fund, raising €28.5 million at first close to focus on early-stage medical and health technology companies in the Netherlands. PureTerra Ventures has introduced its second water-focused fund, anchored by a €10 million commitment from Invest-NL, targeting scalable water treatment technologies for industrial applications. Digital Transformation Capital Partners is also raising a €500 million defense-focused venture fund in Luxembourg, with plans to make approximately 30 investments in European defense startups.

Key Takeaways

Scale and brand are once again determining who can raise at the top end of the market

Flagship fundraising continues to favor the largest, most established managers, with fund sizes creeping higher among firms that combine scale, a long track record, and clear sector focus. The result is a bifurcated market, where only a limited group can consistently raise mega-funds, while mid-scale generalists face a tougher path.

Secondaries are becoming a core allocation

Fundraising momentum across GP-leds, credit secondaries, and real estate secondaries reflects a shift in how LPs view secondaries as a whole. Rather than a tool for liquidity management or portfolio clean-up, secondaries are increasingly underwritten as a strategic allocation, valued for faster deployment, shorter duration, and more controlled risk-adjusted returns.

Product structures are evolving to meet how LPs and wealth capital want to allocate

Managers are moving beyond traditional closed-end funds, expanding into continuation vehicles, evergreen credit, ELTIFs, and interval-style structures. This is less about marginal innovation and more about a structural reset in how private market exposure is packaged, accessed, and scaled across different investor bases.

Capital is concentrating in durable, policy-aligned, and income-oriented strategies

In a more uncertain macro and geopolitical backdrop, investor demand is gravitating toward areas with clearer cash flows and external support. Defense, infrastructure, private credit, and real asset debt are attracting disproportionate attention as LPs prioritize resilience, yield, and regulatory or policy tailwinds over pure cyclicality.

Dakota Marketplace

Dakota is a financial, software, data and media company based in Philadelphia, PA. Dakota’s flagship product, Dakota Marketplace, is a database of LPs, GPs, Private Companies and Public Companies used by thousands of fundraising, deal, and investment teams worldwide to raise capital, source deals, track peers, and access comprehensive data—all in one global platform.

For more information, book a demo of Dakota Marketplace!