Private markets fundraising runs on relationships. But relationships have to start somewhere. For investment firms raising capital in private equity, private credit, real assets, or real estate, 13F data offers a starting point that most capital raisers overlook: a publicly available record of which allocators are already buying structures and strategies adjacent to theirs.

What 13F data actually tells private markets fundraisers

The Form 13F was designed to disclose public equity holdings — not private fund commitments. Private fund investments do not appear in 13F filings. So why does it matter for private markets fundraising?

Because public market behavior is a proxy for private market appetite. An RIA that consistently holds BDCs, senior loan ETFs, closed-end credit funds, or listed infrastructure vehicles has already signaled something important: they are comfortable with the underlying strategy, they have cleared internal compliance hurdles for the structure, and they have allocated client capital to that risk profile. That is a meaningfully warmer starting point than a cold approach to a firm whose preferences are unknown.

Public holdings as a signal of private appetite

The difference between a cold call and a warm one

Traditional prospecting for private markets capital relies heavily on conference introductions, placement agent networks, and referrals. These are slow to build and hard to scale. A 13F-based approach adds a data layer that systematically identifies allocators already expressing interest in adjacent strategies through their public market allocations.

The key distinction is what this data allows you to skip. You do not need to spend the first conversation explaining what private credit is to an RIA that has held five BDCs for three years. The conversation starts further along. The allocator has already done the work of understanding the strategy, justifying it internally, and allocating client capital to it. Your job is to make the case for your specific fund — not the asset class.

A 13F won't show you private fund commitments. It will show you which allocators have already decided they belong in the strategies you're raising.

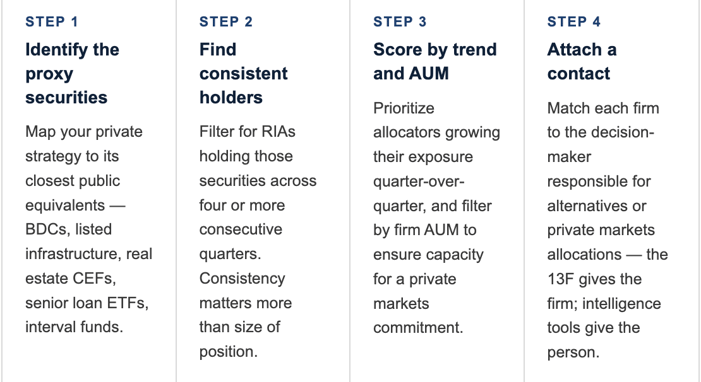

Four steps from raw filing to prioritized prospect

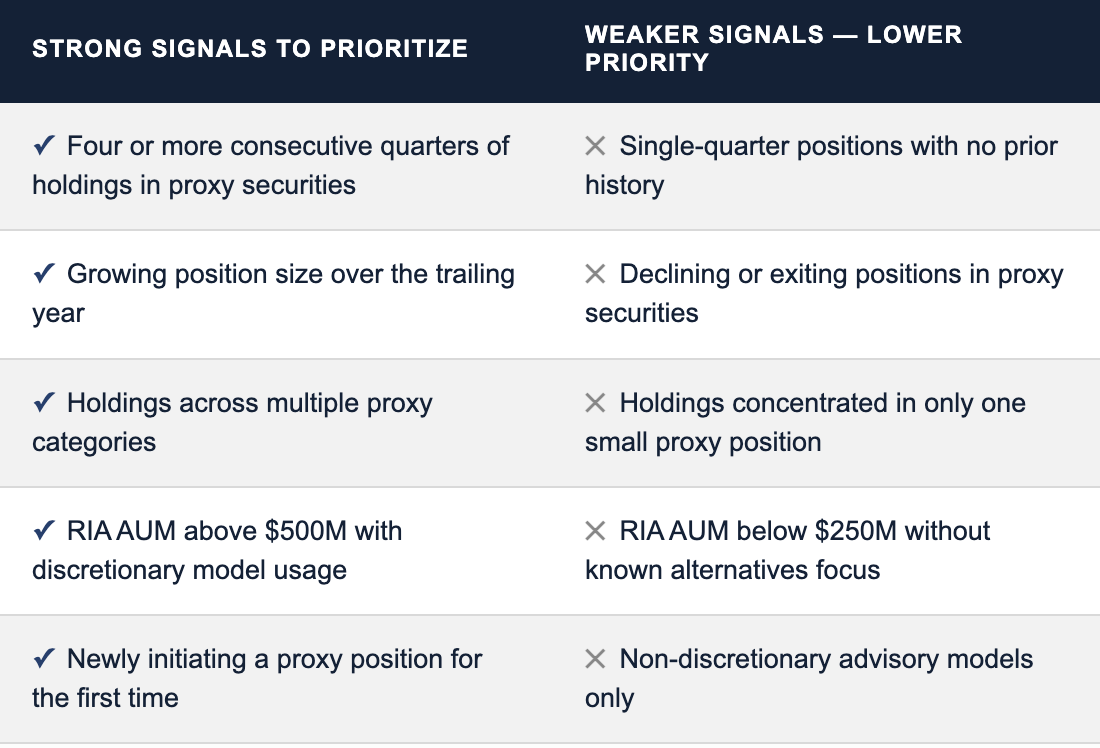

What to look for — and what to ignore

What 13F data can’t tell you

The proxy approach has real limits. Public market holdings reflect one slice of an allocator’s portfolio — an RIA with strong BDC exposure may already be fully committed to private credit and have no capacity for a new fund. The 13F also provides no information on existing private fund relationships, lock-up constraints, or redemption cycles that might affect timing.

And critically, the 13F gives you the firm — not the person. Knowing that a $1.2 billion RIA in Denver holds three BDCs consistently is useful. Knowing which of their advisors leads the alternatives committee, and having a direct contact, is what converts that signal into a meeting.

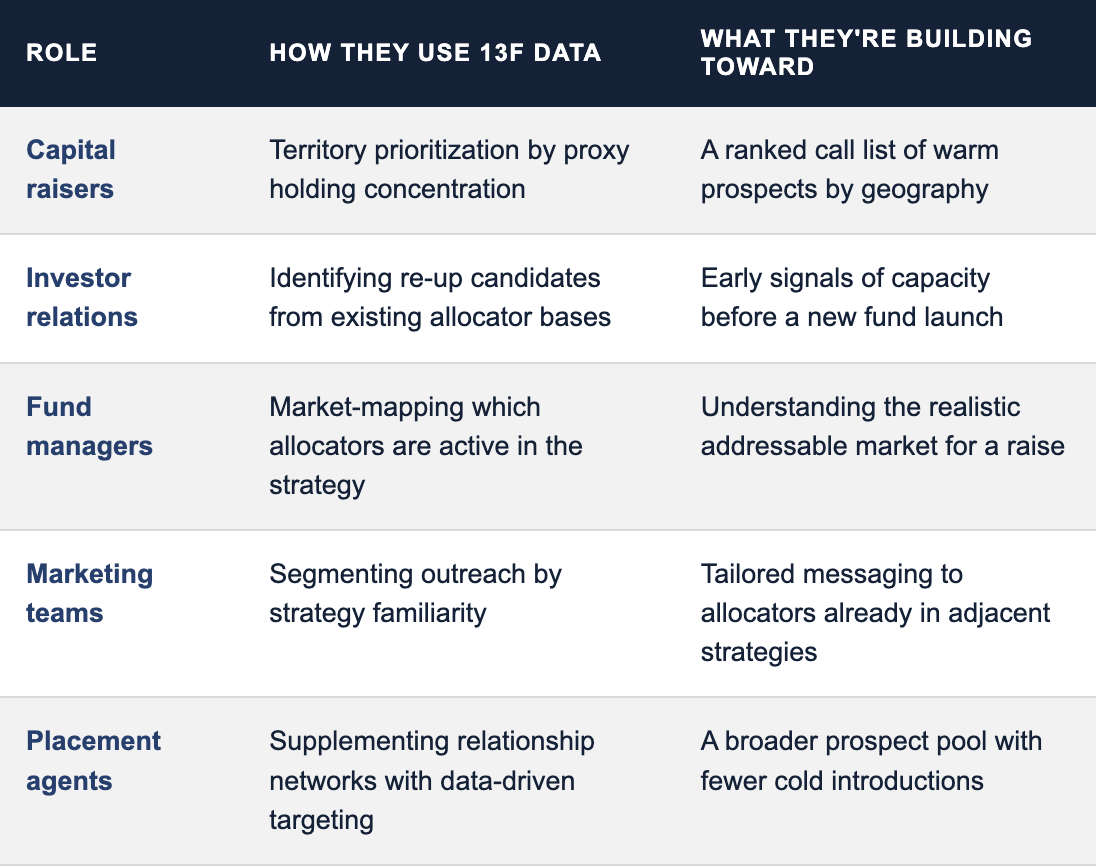

13F-based prospecting across the fundraising team

The list already exists. The work is reading it correctly.

Every quarter, thousands of allocators publicly disclose which strategies they are actively allocating to in public markets. For private markets fundraisers, that disclosure is a map. The allocators expressing the strongest appetite for adjacent strategies in public form are, in most cases, the same allocators most likely to be open to a conversation about private fund exposure.

The 13F does not replace relationship-building. It tells you where to start building.

Dakota Marketplace connects 13F holdings data to 8,000+ verified RIA accounts — with decision-maker contacts, AUM filters, and quarter-over-quarter trend views built in.

Book a demo here!