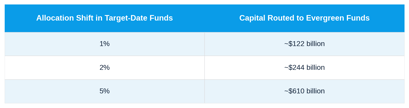

The Department of Labor proposed a safe-harbor rule in March 2026 that would let plan sponsors add evergreen funds to 401(k) lineups without taking on additional fiduciary liability. If finalized, it would clear the largest legal barrier between $12.2 trillion in U.S. defined-contribution assets and the private markets. A 2% shift in target-date fund allocations alone would route $244 billion into evergreen vehicles, more than half the current U.S. evergreen AUM base.

Tracking 450+ evergreen funds through our private markets database, we see that most of the infrastructure to deliver these products inside a 401(k) is already built. The remaining questions are timing, plan sponsor adoption, and which managers are positioned to win the assets when the door opens.

In this article, we walk through the regulatory path that got us here, the math of the opportunity, why evergreens fit when drawdowns don't, what sponsors have already built, the three open questions still in play, and what this means for investment firms and advisors.

The 401(k) Opening

The Regulatory Sequence

The path to 401(k) access has moved faster than most observers expected. In August 2025, an executive order directed federal agencies to expand defined-contribution plan access to alternative investments, and the DOL followed in March 2026 with a proposed rule that gives plan sponsors a process they can follow when adding alternatives to a 401(k) lineup, with protection from fiduciary liability if they do. The proposal is not yet final, with the comment period closing in May 2026 and implementation expected over the next two to three years, but the direction is settled. The question now is execution, and that runs through the target-date fund channel.

The Size of the Opportunity

U.S. defined-contribution plans held $12.2 trillion in assets at the end of 2024, with effectively zero exposure to private markets. The largest concentration of those assets sits in target-date funds, which now collect the majority of new 401(k) contributions. That makes the TDF the single most important conduit for any private markets allocation that follows the rule's finalization.

For context, the current U.S. evergreen market totals $431 billion across 252 registered vehicles. A 2% shift would add more than half the existing market in a single regulatory event, and a 5% shift would more than double it. These are not flow estimates over a decade; they are what a single rebalance across the TDF universe would deliver if plan sponsors execute it.

Why Evergreens Are the Vehicle

Why Evergreens, Not Drawdowns

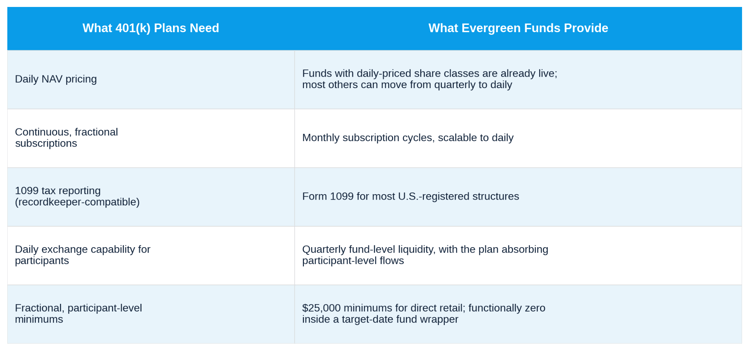

Closed-end drawdown funds are not workable for 401(k) plans, and the reasons are mechanical rather than philosophical. Capital calls, K-1 tax reporting, $250,000 minimums, ten-year lockups, and quarterly-at-best pricing all break against a system that processes daily participant contributions and exchanges across millions of accounts. Evergreen funds were built for the opposite problem.

The unsolved piece is liquidity. A 401(k) participant can exchange their target-date fund daily, but an evergreen fund offers quarterly redemptions capped at 5% of NAV. The reconciliation happens at the plan level: the TDF holds the evergreen position and manages liquidity by netting participant flows against the rest of the portfolio. The participant never sees the gating, which is the whole point of routing alternatives through a TDF wrapper rather than offering them as a standalone option.

The Build Is Mostly Done

Most large managers have been preparing for the rule since the executive order landed in August 2025, and the work falls into three categories that need to come together before the first major plan adoption.

A target-date fund prices its holdings daily, so any evergreen included in a TDF needs to support daily NAV calculation. The largest sponsors are moving from quarterly to monthly to daily for new ERISA-compliant share classes, with the operational systems either live or in final testing. Those ERISA share classes are themselves a meaningful build, carrying lower fees, no performance allocation, and operating terms compatible with ERISA's prohibited-transaction rules, and most major managers have already filed for or launched them.

The third piece, recordkeeper integration, is the most operationally complex. A 401(k) trade routes through a recordkeeper, not directly to a fund sponsor, so building the data pipes between alternative asset managers and the handful of major recordkeepers that run the U.S. plan market is the lift that has been underway for two years. It is also the work that determines who can transact at scale on day one of the final rule.

See every evergreen fund, ERISA filing, and sponsor partnership in one place and book a demo of Dakota Marketplace.

What’s Still in Play

Three Open Questions

Three open questions will shape how this plays out, and the order matters.

-

Plan sponsor adoption speed: Even with a safe harbor, plan sponsors move slowly, and the first wave will be large corporate plans with sophisticated investment committees and an OCIO already running the lineup. Mid-market and smaller plans will follow only when consultants like Mercer, Aon, and Callan build standard recommendations, which historically takes a year or two after the underlying rule lands.

-

Litigation risk: The safe harbor reduces fiduciary exposure but does not eliminate it, and plaintiffs' attorneys have built a practice around 401(k) fee litigation that will not pause for this rule. The fee load on evergreen products, even after ERISA share classes compress it, will draw scrutiny, and filings within twelve months of the first major plan adoption should be expected.

-

Which sponsors win the allocation: The TDF market is concentrated among a handful of large asset managers, including BlackRock, Vanguard, Fidelity, T. Rowe Price, State Street, and Capital Group, and their decisions about which private markets sponsors to include will route hundreds of billions of dollars. The partnerships forming right now are structured exactly for this distribution. T. Rowe Price filed a joint interval fund with Goldman Sachs. Capital Group, the parent of American Funds, partnered with KKR. Lincoln Financial partnered with Bain Capital. Each pairing puts a large traditional asset manager with established 401(k) distribution alongside an alternatives specialist with product, and the timing of these tie-ups is not a coincidence.

Implications for Investment Firms and Advisors

For investment firms running an evergreen, the work is being done now. Plan sponsor due diligence cycles run six to twelve months, so sponsors that want to be in the first wave of TDF allocations need their ERISA share class, daily NAV capability, and recordkeeper relationships in place before the rule is finalized, not after. Sponsors that wait until the final rule lands will be raising into a market where the early winners already have shelf space, and that gap is hard to close once a TDF manager has signed off on a competitor's vehicle.

For advisors, the more immediate question is what to tell clients. Participants in plans that adopt these products will be reading headlines about private markets coming to 401(k)s within the next year, and the conversation about what evergreen funds are, what they are not, and how the 5% quarterly redemption cap interacts with daily-priced TDF exposure is going to come up. Advisors who can answer it cleanly will earn trust on harder questions later. The full background on how the evergreen market is structured today, including the return dispersion data, the structural risks, and the partnership model driving new fund launches, is in our May 2026 Evergreen Market Landscape report.

Tracking the Pipeline

We track every N-2 filing, ERISA-compliant share class launch, and sponsor partnership across 450+ evergreen funds in Dakota Marketplace, including 100+ vehicles no prior database had identified as evergreen.

Every record is sourced from public regulatory filings and standardized across private equity, private credit, real estate, and hybrid strategies. Filter by sponsor, strategy, AUM, or filing date to see who is positioned for DC plan distribution, and who is still building toward it.

Book a demo of Dakota Marketplace to see.