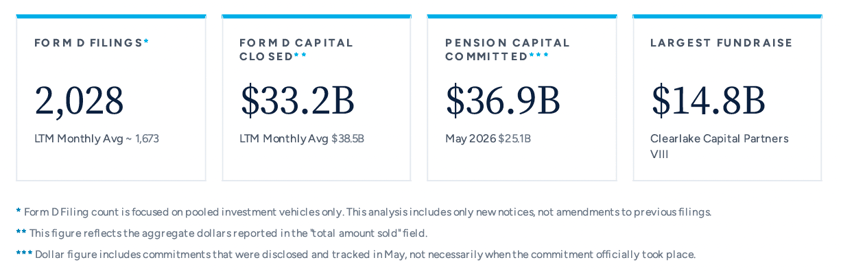

June Fundraising Monitor

Form D filings by strategy and asset class are searchable and filterable inside Dakota Marketplace the day they're recorded, well before they show up in monthly recap like this one. Book a demo to see June's filings filtered to your specific strategy.

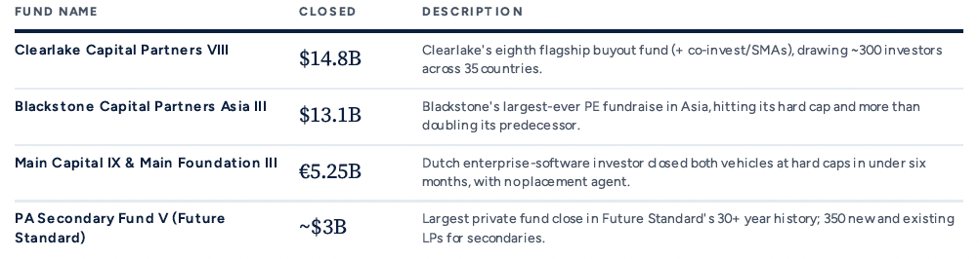

Private Equity

June saw a strong month for large-cap and mid-market buyout closes, with several flagship funds hitting hard caps well above their initial targets. Clearlake's $14.8B close and Blackstone's record $13.1B Asia raise led the month, both drawing broad international LP bases and exceeding predecessor sizes by meaningful margins. The mid-market also showed strength, with Norvestor X closing three months after launch at its €2B hard cap and Longship Fund IV hitting its hard cap in just 11 weeks. Continuation vehicles remained active, with Capital A, Abry, and Palladio all competing GP-led secondaries, while Francisco Partners approached final close on a combined $18B+ raise across two vehicles. On the launch side, Carlyle began marketing its ninth flagship at $15B alongside a new dedicated defense fund, and TJC filed for an $8.5B vehicle - signals that the large-cap pipeline remains well-stocked heading into H2.

Notable Fund Closes

Every allocator behind these closes - family offices, pensions, and consultants alike - is searchable by commitment size, asset class, and manager review timeline inside Dakota Marketplace.

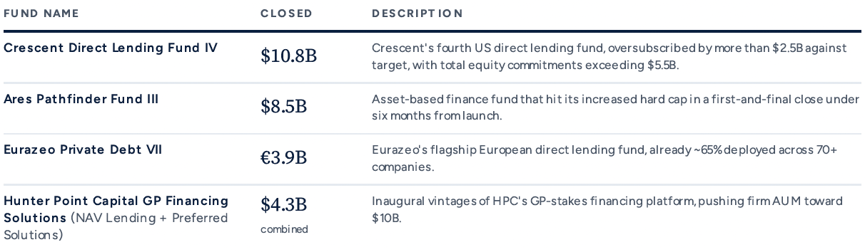

Private Credit

Private credit posted one of its strongest months of 2026, with flagship direct lending and asset-based finance vehicles closing well above target across the US and Europe. Crescent's $10.8B Fund IV and Ares Pathfinder III's $8.5B first-and-final close both reflect continued robust allocator demand for senior secured strategies, with Pathfinder III oversubscribed against an already-increased hard cap in under six months. Eurazeo's €3.9B European direct lending close further illustrates the cross-border appetite for the asset class, with international investors (particularly from North America and Asia) accounting for more than 60% of commitments. GP financing continued to emerge as a distinct sub-strategy, with Hunter Point Capital closing $4.3B across its inaugural NAV lending and preferred solutions vehicles. On the liquidity side, non-traded BDCs faced mounting redemption pressure: both Ares Strategic Income Fund and the Partners Group Global Value SICAV capped quarterly withdrawals at 5% of NAV, a dynamic worth watching as retail-channel vehicles continue to scale.

Notable Fund Closes

Insurance companies, pensions, and other allocators increasing private credit exposure are tagged and filterable by strategy inside Dakota Marketplace, along with the specific decision-makers reviewing each mandate.

Real Assets

On the infrastructure side, EQT set a €21B target for its next flagship and Goldman Sachs reached ~75% of its $4B West Street Infrastructure V target at first close, anchored by its QScale data center acquisition. Copenhagen Infrastructure Partners quietly launched CI VI targeting approximately €16B. Conifer Infrastructure Partners closed its debut fund at a $900M hard cap, nearly double its $500M target, completing the raise in a single close in under five months. In real estate, logistics and residential remained the strategies of choice for institutional capital — Greystar's European residential fund closed 76% above its predecessor, Bridge Logistics exceeded its $1B target with Apollo backing, and Kotak's India real estate fund drew a sixth consecutive ADIA commitment alongside a landmark first investment from NPS Korea. The nature-based solutions space also saw activity, with Finance Earth's Big Nature Impact Fund and Ardian's Averrhoa NBS vehicle each completing early closes backed by insurance companies and corporate anchor investors.

Notable Fund Closes

ADIA, NPS Korea, and every other sovereign and pension allocator active in real assets this month are tracked with allocation history and current review status inside Dakota Marketplace.

ADIA, NPS Korea, and every other sovereign and pension allocator active in real assets this month are tracked with allocation history and current review status inside Dakota Marketplace.

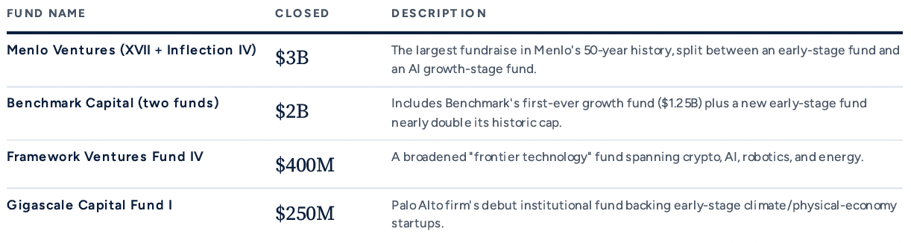

Venture Capital

June was a big month for venture fundraising, defined by a generational step-up in fund sizes at established firms and a clear thematic concentration around artificial intelligence. Benchmark's $2B raise and Menlo's $3B dual-fund close both reflect a broader pattern of top-tier VCs expanding their scope to capture AI value across the lifecycle, from early-stage infrastructure bets to late-stage compounding. The AI theme extended into climate and deep tech, with Gigascale's $250M debut close backing physical economy startups and Deep33's $200M debut exceeding its target with a US-Israel AI infrastructure focus. Framework's fourth fund broadened its mandate beyond crypto to encompass AI, robotics, and energy — a signal that the frontier technology category is consolidating. Earlier in the market, a high volume of sub-$100M debut and emerging manager closes continued across Europe, Asia, and Africa, indicating the seed and pre-seed layer remains active globally despite the concentration of allocator dollars at the top.

Notable Fund Closes

The allocators backing these AI-focused vehicles, and their historical venture allocation patterns, are searchable by check size and stage preference inside Dakota Marketplace.

Key Takeaways

1. LP demand remains strong at the top, but concentration is intensifying.

The largest funds in June closed at or above hard cap, often in compressed timeframes — Norvestor in three months, Longship in 11 weeks, Ares Pathfinder in under six months. But this strength is not evenly distributed. Astorg's ninth flagship reportedly struggled to reach a first close after six months in market, and several mid-tier managers are taking longer or scaling back targets. Capital is flowing decisively to brand-name managers with strong track records.

2. Asia and emerging markets are attracting fresh institutional conviction.

Blackstone's record $13.1B Asia PE raise, Kotak's landmark NPS Korea commitment, MUFG's India VC push, and multiple first-close vehicles across Southeast Asia, India, and Africa point to a meaningful uptick in cross-border allocator interest in non-US markets. India in particular emerged as a recurring destination, appearing across PE, VC, private credit, and real estate fundraises in a single month.

3. AI is shaping fund strategy across every asset class.

The influence of AI extended well beyond venture capital in June. Infrastructure managers anchored first closes to data center acquisitions (Goldman's QScale deal), private credit vehicles oriented around AI infrastructure financing (KKR's Helix platform launching with $10B+), and buyout funds explicitly cited AI infrastructure and energy security as emerging themes. AI is no longer a VC-specific thesis — it is reshaping mandate construction across the alternatives landscape.

Dakota Marketplace

Dakota is a financial, software, data and media company based in Philadelphia, PA. Dakota's flagship product, Dakota Marketplace, is a database of allocators, investment firms, private companies, and public companies used by thousands of fundraising, deal, and investment teams worldwide to raise capital, source deals, track peers, and access comprehensive data — all in one global platform.

For more information, book a demo of Dakota Marketplace!