May public pension disclosures tracked by Dakota expanded materially from the prior month, with approximately $24.85B in reported private market commitments across 185 deals, compared with $15.95B across 128 deals in April. The expansion in tracked volume was driven in meaningful part by non-US allocator CPP Investments, which accounted for more than $6B of the month’s total across 20 commitments.

Private real estate staged a sharp recovery, reclaiming its position as one of the top-two asset classes by dollar volume alongside private equity. Hedge funds and liquid alternatives also expanded substantially, anchored by several large multi-strategy and macro allocations from North Carolina Retirement Systems, while private credit relinquished its April lead back to private equity.

Below is a breakdown of commitments by allocator and strategy, with a focus on the most notable tracked allocations with month-to-month analysis.

May’s tracked disclosures were dominated by CPP Investments at $6.36B, followed closely by North Carolina Retirement at $6.06B. In terms of deal volume, Florida State Board of Administration – also among the top allocators with $2.1B in commitments – tied with CPP at 20 commitments disclosed last month. The concentration profile differed markedly from April, when no single plan exceeded $2.5B. In May, the top two allocators alone accounted for roughly half of total tracked volume, a dynamic more reminiscent of March’s CalPERS-heavy dataset than April’s diffuse mix.

Further down the rankings, New Mexico State Investment Council posted $861M across nine commitments, anchored by a $550M special situations allocation to Silver Rock Lobo A. Mass PRIM and Kansas Public Employees Retirement System also contributed meaningfully, with $781M and $745M, respectively, each deploying across diversified private equity and real estate mandates.

Eighty-two of the 185 total tracked deals were above $100M, placed by 16 distinct allocators. The largest individual allocation in the May dataset was CPP Investments’ $1.3B commitment to Japan DC Partners I in opportunistic real estate, followed by three $1B commitments: CPP’s Blackstone Private Credit Fund (BCRED) in direct lending, and North Carolina Retirement Systems’ ARC Infra SMA, L.P. in value-add infrastructure and Gladius Arx Fund in multi-strategy hedge funds.

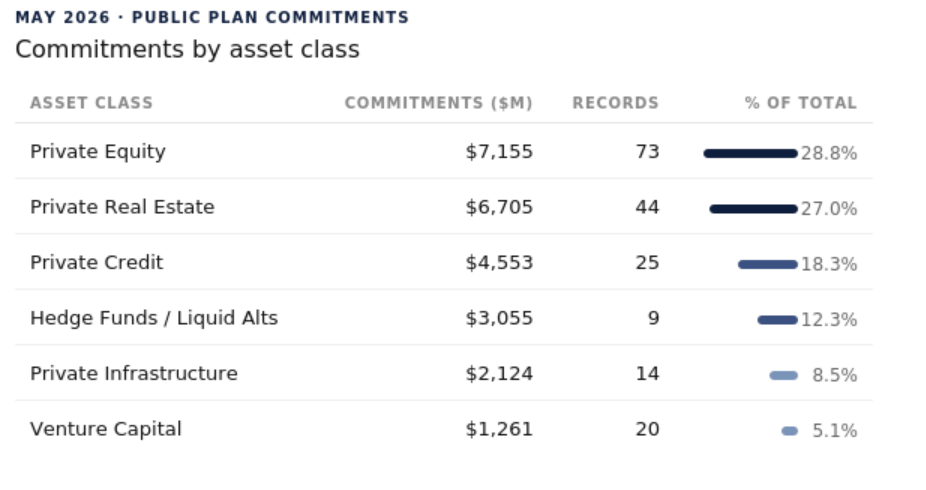

Asset Classes

Private equity led all asset classes in May at $7.16B across 73 tracked deals, representing 28.8% of total disclosed commitments by dollar value – a sharp reversal from April, when private credit held the top position. The advance reflects both a higher deal count (up from 44 in April) and larger average ticket sizes, with CPP Investments and North Carolina Retirement Systems each contributing sizable buyout and growth equity allocations. Private real estate followed at approximately $6.71B across 44 commitments, recovering from April’s $1.83B as CPP’s Japan-focused disclosures and North Carolina’s commercial real estate commitments drove the rebound.

Private credit stepped back to $4.55B across 25 deals versus $5.38B in April, though deal count held relatively firm. Hedge funds and liquid alternatives more than doubled from $1.3B to $3.06B, with North Carolina’s multi-strategy and macro mandates – including a combined $1.9B across Gladius Arx, AG Cataloochee, and Balyasny vehicles – accounting for the bulk of the increase. Private infrastructure nearly doubled to $2.12B across 14 deals from $1.09B, with large core and value-add allocations from North Carolina, Connecticut, and Kansas contributing to the step-up.

Venture capital was essentially flat month-over-month at $1.26B across 20 deals versus $1.18B across 19 in April. Real assets were not represented as a distinct asset class in May’s tracked dataset, compared with $230M across four commitments in April, while multi-asset activity also dropped out of the disclosed universe relative to April’s single $300M GTAA mandate from Virginia Retirement.

Dakota Marketplace captures public pension disclosures across private equity, private credit, real estate, infrastructure, and more — so you always know where capital is moving before your competitors do. Talk to an expert here.

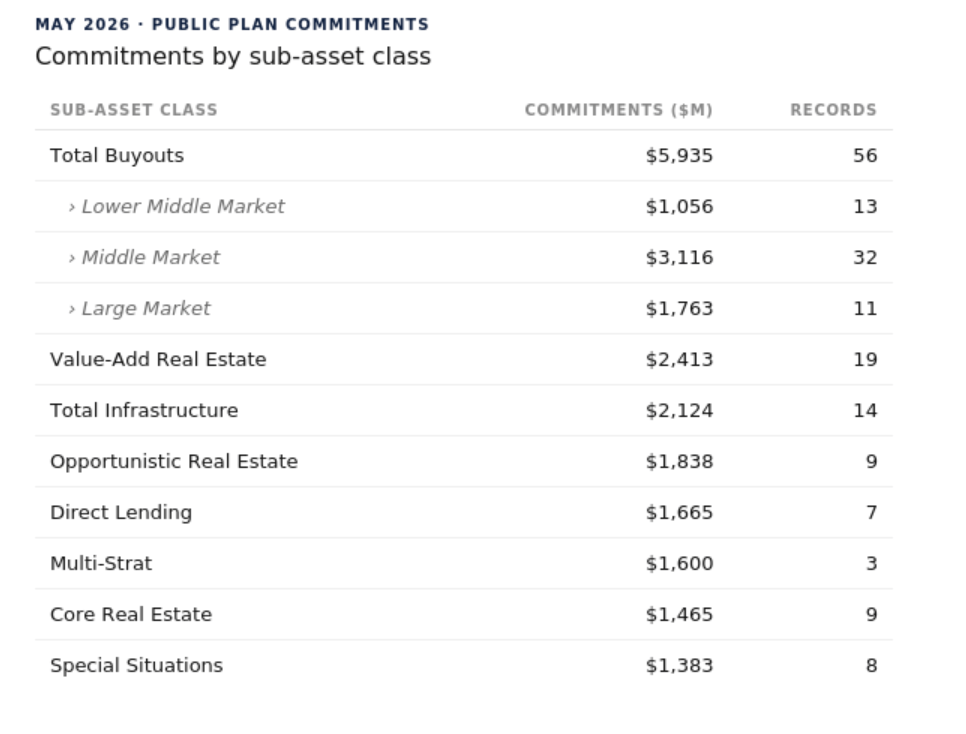

Sub-Asset Classes

May’s private equity disclosures were defined by a broad-based buyout recovery, with total buyout commitments reaching $5.93B across 56 tracked deals – nearly triple April’s $1.97B. The composition shifted upmarket: large buyouts accounted for $1.76B, a more than fivefold increase from $335M, while the lower middle-market segment also expanded significantly to $1.06B from $200M. Middle-market activity remained the dominant sub-bucket at $3.12B, but the proportional gains were most pronounced up and down market. Growth equity tracked at $905.7M across nine deals, more than double April’s $419M, though the increase was distributed across a wider set of smaller commitments rather than anchored by a single large position.

The private credit picture was more mixed. Direct lending climbed to $1.67B from $1.26B, with CPP’s $1B BCRED commitment doing most of the lifting. Opportunistic credit, which had been April’s standout sub-category at $1.65B on the back of two large allocations from Indiana’s state pension, pulled back to $790M. Special situations was the clearest growth story within credit, rising to $1.38B across eight deals from $650M across three.

Within real estate, all three sub-categories moved in the same upward direction after April’s broad pullback. Value-add led in absolute terms at $2.41B across 19 deals, while opportunistic real estate reached $1.84B due to heavy CPP influence. Core real estate more than doubled to $1.46B across nine deals from $721M across just two in April.

Meanwhile, co-investments contracted sharply to $522M across nine deals from $1.32B, and secondary private equity was essentially absent at $7.5M – a single University of Vermont allocation – compared with $1.16B in April. In infrastructure, the notable development was the return of core infrastructure at $600M, a sub-category with no meaningful representation in April, as North Carolina’s ArcLight commitment and Connecticut’s AxInfra allocation drove the category back into the dataset. Multi-strategy within hedge funds jumped to $1.6B from $307.5M, entirely attributable to North Carolina’s concentrated positioning across three separate vehicles.

This analysis is based on Dakota Marketplace data capturing pension commitments across private equity, private credit, private real estate, private infrastructure, real assets, venture capital, hedge funds/liquid alternatives, and multi-asset strategies, sourced from public filings and other reports published during the month.

To explore more commitments made my public pension funds, book a demo of Dakota Marketplace.