Wirehouses and independent broker-dealers (IBDs) remain core pillars of the U.S. wealth management distribution ecosystem. While the registered investment advisor (RIA) channel has attracted significant attention over the past decade due to rapid growth and private equity investment, wirehouses and broker-dealers still control trillions of dollars in client assets and maintain some of the largest advisor networks in the industry.

The traditional wirehouse model, represented by Morgan Stanley, Merrill Lynch (Bank of America), UBS Wealth Management, and Wells Fargo Advisors, operates as an integrated wealth platform that combines advisory services with banking, lending, capital markets access, and institutional research capabilities. Together, these firms control an estimated 20% of total U.S. wealth management assets according to Boston Consulting Group.

The IBD channel has also evolved significantly. Firms such as LPL Financial, Ameriprise Financial, Osaic, and Cetera provide advisors with greater autonomy while maintaining centralized compliance, technology infrastructure, and product access. Although the number of broker-dealers has declined due to consolidation and rising regulatory complexity, assets across the channel have continued to grow as larger platforms capture increasing market share.

Several structural forces are reshaping both channels, including advisor succession dynamics, competition for experienced advisors, and rising technology investment. While the industry continues to move toward greater independence and open-architecture, wirehouses and broker-dealers remain critical intermediaries between asset managers and investors.

Key Industry Insights

- Wirehouses retain significant market share: The four major wirehouses are estimated to control one-fifth of U.S. wealth management assets and continue to dominate high-net-worth and ultra-high-net-worth client segments through integrated banking and advisory platforms.

- Scale is becoming critical in the IBD channel: Rising compliance costs, technology investment, and recruiting expenses are pushing the industry toward fewer but significantly larger platforms.

- Advisor independence will continue to expand: Many advisors are migrating toward independent platforms that offer flexible compensation structures, ownership economics, and open-architecture product access.

- Alternatives are moving deeper into wealth portfolios: Wirehouses and broker-dealers are expanding access to private equity, private credit, and other private market strategies across high-net-worth client segments.

- Technology is reshaping advisor productivity: Firms are investing heavily in artificial intelligence, integrated planning tools, and digital client engagement platforms to improve advisor efficiency and client service.

- Advisor succession will drive recruiting and consolidation: A large cohort of advisors approaching retirement is increasing competition for experienced advisors and accelerating succession planning across the industry.

The Wealth Management Distribution Landscape

The U.S. wealth management industry is composed of several advisor distribution models that differ in operating structure, client service approach, and advisor economics. Among advisor-led platforms, wirehouses and broker-dealers represent two of the most influential channels.

Wirehouses operate as large centralized institutions embedded within global banking organizations, while IBDs provide infrastructure and oversight for advisors operating more autonomous practices. Although both models serve similar client segments, they differ significantly in advisor compensation structures, operational flexibility, and product architecture.

Historically, wirehouses dominated the advisor-led market through their scale, brand recognition, and integrated financial services capabilities. However, the industry has gradually shifted toward greater advisor independence as technology has lowered barriers to entry and enabled smaller firms to offer sophisticated investment and planning services.

IBDs emerged as an intermediary model between traditional wirehouses and fully independent RIAs. These platforms provide compliance oversight, technology infrastructure, and product access while allowing advisors to operate their own businesses with greater flexibility.

Despite the growth of independent advisory models, both wirehouses and broker-dealers continue to command enormous scale and remain essential distribution channels for asset managers seeking access to the wealth market.

Wirehouses

The traditional wirehouse model refers to large national wealth management firms characterized by centralized distribution, extensive branch networks, and integrated product platforms. Today, the four firms most commonly described as wirehouses are Morgan Stanley, Merrill Lynch (Bank of America), UBS Wealth Management, and Wells Fargo Advisors.

These institutions remain among the most powerful wealth management platforms globally. Their affiliation with large banking organizations allows them to deliver a broad suite of financial services that extend beyond traditional investment advisory. Advisors can provide integrated solutions combining portfolio management, lending, banking services, estate planning, and access to capital markets.

Centralized research platforms, chief investment offices, and internal model portfolios help advisors scale investment recommendations across large client bases. These institutional resources have historically given wirehouses a significant advantage in serving high-net-worth and ultra-high-net-worth clients.

However, the traditional wirehouse model faces increasing competition from independent advisory platforms. RIAs and IBDs often provide advisors with greater autonomy and ownership economics. Advances in financial technology have also reduced many of the infrastructure advantages historically associated with large institutions.

In response, wirehouses are investing heavily in technology modernization, digital client platforms, and advisor productivity tools while expanding capabilities in areas such as lending, alternatives, and integrated financial planning.

The Big Four Wirehouses

Merrill Lynch (Bank of America)

Merrill Lynch serves as Bank of America’s primary wirehouse platform and operates within the firm’s Global Wealth and Investment Management (GWIM) division alongside Bank of America Private Bank. Merrill Wealth Management primarily serves high-net-worth clients with approximately $1 million to $10 million in investable assets, while the Private Bank focuses on ultra-high-net-worth households with more than $10 million in assets.

The Merrill platform oversees approximately $3.9 trillion in client balances, including roughly $1.7 trillion in assets under management, and serves approximately 750,000 client households through 546 offices across 98 markets. The business operates through a nationwide branch-based advisory model typical of traditional wirehouses.

A distinguishing feature of Merrill’s platform is its integration with Bank of America’s broader financial services ecosystem, enabling advisors to provide clients with coordinated investment management, banking, and lending solutions.

Source: Bank of America 2025 Investor Day Presentation – Global Wealth & Investment Management

Morgan Stanley

Morgan Stanley Wealth Management operates one of the largest advisor-led wealth platforms globally. The division oversees approximately $7.4 trillion in client assets, including $5.7 trillion in advisor-led assets and $2.7 trillion in fee-based assets, supported by a network of roughly 18,000 financial advisors.

The platform has experienced significant growth in recent years, generating approximately $830 billion in net new assets over the past three years. Morgan Stanley has expanded the scope of its wealth management platform through acquisitions and technology investments.

The firm’s acquisition of E*Trade added a large self-directed brokerage channel that complements its traditional full-service advisory model. In parallel, the firm has invested in artificial intelligence and digital tools aimed at improving advisor productivity and enhancing client engagement.

Source: Morgan Stanley Form 10-K (December 2025)

UBS

UBS operates a large global wealth management platform with a significant presence in the United States through UBS Wealth Management Americas, which functions as the firm’s primary wirehouse platform in the region. The business primarily serves high-net-worth and ultra-high-net-worth clients and emphasizes advisory services that incorporate investment management, financial planning, and access to alternative investments.

Globally, UBS oversees approximately $6.6 trillion in invested assets. Within the Americas division, the firm employed approximately 5,779 financial advisors as of the third quarter of 2025, with average client assets of roughly $353 million per advisor, reflecting the firm’s focus on larger client relationships.

UBS’s wealth platform is supported by the firm’s global investment capabilities and research infrastructure, enabling advisors to deliver portfolio construction and asset allocation strategies across public and private markets.

Source: UBS disclosures and website

Wells Fargo

Wells Fargo Advisors represents the firm’s primary wirehouse brokerage platform and operates within Wells Fargo’s Wealth and Investment Management division. The business oversees approximately $2.5 trillion in client assets, including $1.1 trillion in advisory assets and $1.4 trillion in brokerage assets and deposits.

The platform is supported by approximately 13,200 financial advisors operating through a nationwide branch network. Wells Fargo Advisors follows a traditional wirehouse model centered on advisor-led brokerage and advisory relationships with affluent and high-net-worth households.

The firm continues to invest in advisor technology and digital platform capabilities intended to improve advisor efficiency and support client service across its national advisor network.

Source: Wells Fargo 4Q25 Investor Presentation

Independent Broker-Dealers

IBDs provide infrastructure, compliance oversight, and platform access to advisors who operate with greater autonomy than their wirehouse counterparts. Advisors affiliated with IBDs typically retain control over branding, staffing, and practice management while leveraging centralized supervision, technology infrastructure, and product access.

The independent model has expanded significantly over the past decade as advisors seek greater ownership economics, flexible compensation structures, and open-architecture product platforms. However, the structure of the industry has evolved as regulatory complexity and technology investment requirements have increased the importance of scale.

Industry Consolidation

Consolidation in the independent broker-dealer (IBD) channel continues, although it has generally been less active than the rapid consolidation observed in the RIA market in recent years. At the same time, some broker-dealers are adopting hybrid growth strategies by acquiring independent RIAs and integrating advisory capabilities into their platforms. While rising compliance costs, technology investment requirements, and advisor recruiting pressures are pushing firms to pursue greater scale, many IBDs remain relatively stable due to long-standing advisor networks and established clearing relationships.

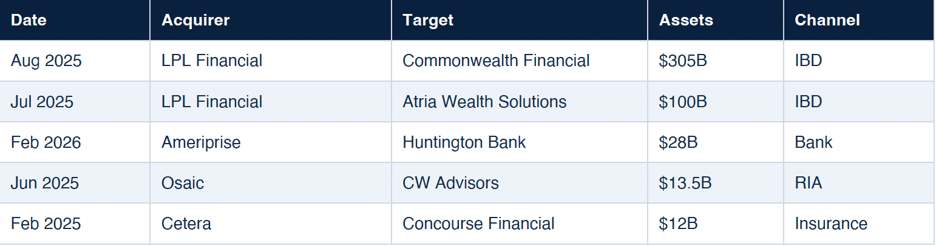

Major IBD / Wealth Platform Transactions

Recent transactions highlight how the largest broker-dealer platforms are selectively expanding through acquisitions across multiple channels, including broker-dealers, RIAs, banks, and insurance-affiliated networks.

Among the most notable deals, LPL Financial’s $2.7 billion acquisition of Commonwealth Financial Network in 2025 added roughly 3,000 advisors and more than $300 billion in client assets. The transaction reinforced LPL’s position as the largest independent broker-dealer and illustrates how leading firms are using acquisitions to strengthen scale even as consolidation in the IBD channel remains more measured than in the RIA market.

Several structural factors are driving consolidation within the broker-dealer industry. Regulatory requirements continue to increase operational complexity, while technology investment and advisor recruiting costs have risen significantly. These pressures have reinforced the importance of scale as larger platforms are better positioned to spread technology, compliance, and operational costs across large advisor networks.

Industry Structure and Asset Growth

Although the number of broker-dealers has declined over the past decade, the industry has continued to grow in terms of total client assets. This dynamic reflects both market performance and the broader industry shift from transaction-based brokerage to fee-based advisory relationships.

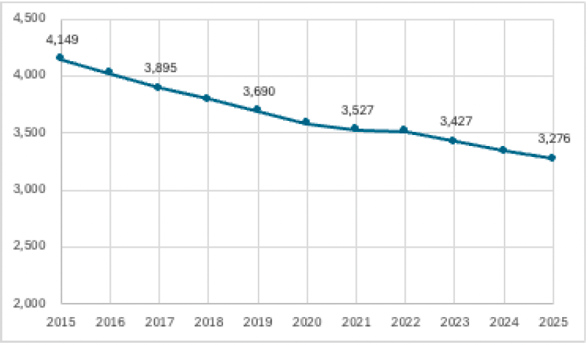

Number of Independent Broker-Dealers

Per FINRA/SEC Data. Broker-Dealer Activity in the United States June2025.

The number of IBDs declined from 4,149 firms in 2015 to approximately 3,276 in 2025, representing a reduction of more than 20% over the past decade.

While the number of broker-dealers has declined, total client assets within the channel have continued to rise.

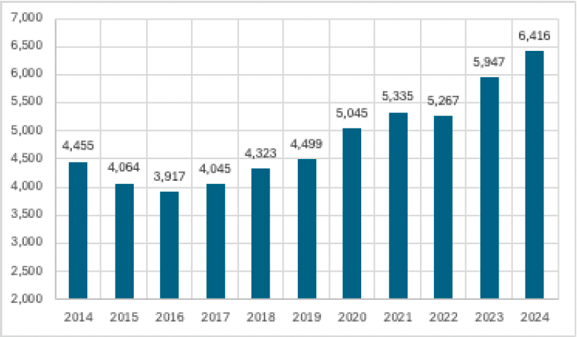

AUM in the IBD Channel

Per FINRA/SEC Data. Broker-Dealer Activity in the United States June2025.

Industry assets increased from approximately $4.5 trillion in 2014 to more than $6.4 trillion in 2024, reflecting both market appreciation and the shift toward fee-based advisory accounts.

This divergence between declining firm counts and rising assets highlights a structural shift in the industry. Broker-dealer assets are increasingly concentrated among fewer but significantly larger platforms.

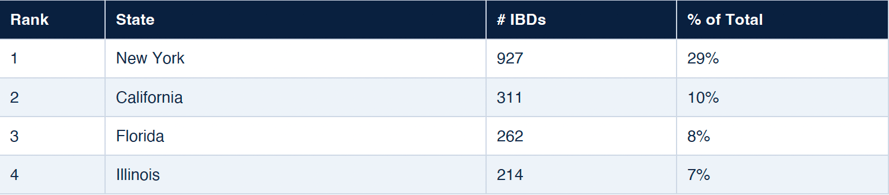

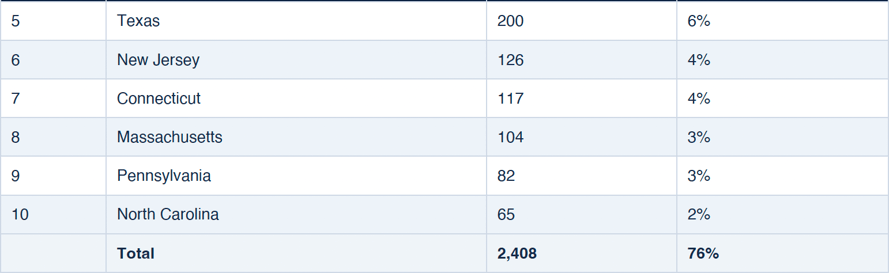

Geographic Distribution of Broker-Dealers

IBDs remain concentrated in traditional financial centers, particularly along the East Coast and in large metropolitan markets. New York continues to represent the largest concentration of broker-dealers in the United States, reflecting the state’s long-standing role as the center of the U.S. financial industry.

However, regional dynamics within the industry are gradually shifting. Several states with favorable tax environments and growing retiree populations have seen increased activity from wealth management firms and advisors. Florida in particular has become an increasingly important hub for wealth management businesses. Population growth, wealth migration, and a favorable regulatory environment have contributed to the expansion of financial advisory practices in the state.

These geographic trends reflect broader demographic shifts within the wealth management industry. As high-net-worth individuals relocate to lower-tax states and retirement destinations, advisory practices and broker-dealer offices often follow their client bases.

Per FINRA/SEC Data. Broker-Dealer Activity in the United States June2025.

New York remains the dominant state for IBDs, accounting for nearly one-third of the national total. Several historically large markets have experienced declines over the past decade as consolidation and regulatory costs have pressured smaller firms.

California has also seen a meaningful reduction in broker-dealer firms despite remaining the second largest state in the industry. In contrast, Florida has experienced growth in the number of firms, reflecting broader migration trends among both advisors and wealthy households.

This distribution illustrates the industry’s continued concentration in major financial centers while also highlighting the increasing importance of states such as Florida and Texas as emerging wealth management hubs.

Scale of Leading Broker-Dealer Platforms

The IBD landscape is increasingly dominated by a small group of national platforms that support tens of thousands of advisors and oversee trillions of dollars in client assets. Firms such as LPL Financial, Ameriprise Financial, Osaic, and Cetera Financial Group have built large national networks that provide advisors with extensive technology, compliance support, and product access.

Scale has become an important competitive advantage within the broker-dealer channel. Large platforms are able to invest heavily in technology infrastructure, compliance systems, cybersecurity programs, and advisor support services. These investments allow firms to deliver integrated advisor workstations, portfolio management tools, financial planning software, and client reporting capabilities that would be difficult for smaller firms to build independently.

LPL Financial remains the largest IBD in the United States by assets and advisor count. The firm supports more than 32,000 advisors and oversees more than $2 trillion in client assets. The firm’s size allows the platform to invest heavily in technology infrastructure, model portfolio programs, and advisor transition support.

Other large platforms have adopted similar strategies. Ameriprise Financial has emphasized integrated wealth management capabilities that combine brokerage services with financial planning and asset management. Osaic and Cetera Financial Group have expanded through acquisitions and advisor recruitment while investing in centralized technology platforms and expanded product offerings.

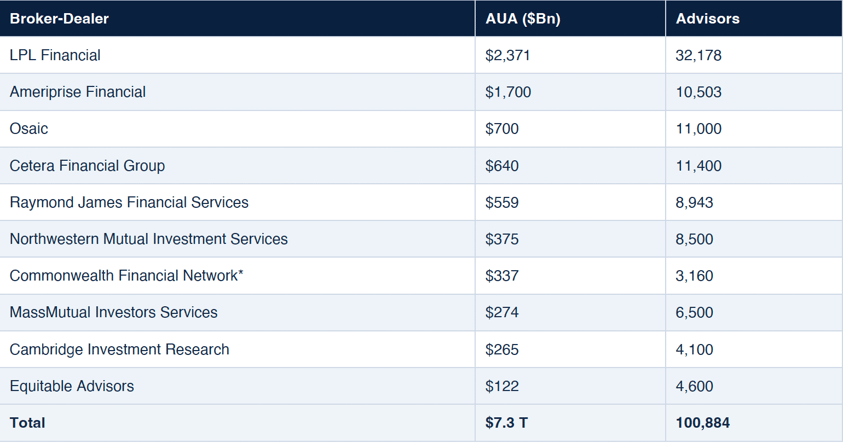

Largest Independent Broker-Dealers

Per Dakota analysis via firm websites and industry reports. Commonwealth Financial Network was acquired by LPL Financial in August 2025.

The top ten IBDs collectively oversee approximately $7.3 trillion in assets under administration across more than 100,000 financial advisors. This concentration illustrates the growing divide between national “super-platforms” and smaller regional broker-dealers.

Large platforms benefit from significant economies of scale. Fixed costs associated with compliance, cybersecurity, regulatory reporting, and technology development can be spread across thousands of advisors and trillions of dollars in client assets. As a result, the largest firms are often better positioned to invest in platform enhancements, advisor recruiting packages, and expanded product shelves.

These firms increasingly operate as full-service wealth platforms rather than traditional brokerage networks. Advisors affiliated with large broker-dealers can access financial planning software, portfolio management tools, insurance products, lending solutions, and private market investments through a single platform. This broader capabilities set allows advisors to deliver more comprehensive wealth management services while maintaining independence from large bank-affiliated firms.

Evolution of the Broker-Dealer Platform

IBDs are expanding their capabilities as they compete more directly with both RIAs and wirehouse platforms. Historically, broker-dealers focused primarily on brokerage services and commission-based investment products. Today, many firms are repositioning themselves as comprehensive wealth management platforms.

A key component of this evolution has been the expansion of fee-based advisory programs. Many broker-dealers now offer advisors the ability to operate hybrid practices that combine brokerage services with fiduciary advisory relationships. These hybrid models allow advisors to provide discretionary portfolio management and financial planning while maintaining access to traditional brokerage products.

Platform modernization has also become a central priority. Modern broker-dealer platforms increasingly offer integrated advisor workstations that combine client relationship management systems, portfolio management tools, financial planning software, and reporting capabilities. These integrated systems help advisors manage their practices more efficiently while improving the client experience.

In addition, broker-dealers have expanded their product shelves to include a broader range of investment solutions. Advisors can now access model portfolios, managed accounts, insurance products, lending programs, and private market investments through a single platform. These capabilities allow advisors to deliver more comprehensive financial planning and investment management services to their clients.

Distribution Dynamics Across Wealth Channels

Asset managers typically approach distribution across wealth management channels differently depending on how products are approved and adopted within each platform. Wirehouses and independent broker-dealers operate through different product approval structures, creating distinct pathways for bringing investment strategies to market.

Wirehouses such as Morgan Stanley, Merrill Lynch, UBS, and Wells Fargo generally rely on centralized due diligence and platform approval processes. Investment strategies are typically reviewed by internal research teams and product committees before they are made available to advisors. This institutional approval process can be rigorous and competitive, but successful platform placement can provide access to thousands of advisors across a national network.

Independent broker-dealer platforms operate with a more decentralized structure. While many large firms maintain research teams and approved product lists, individual advisors often retain greater flexibility in selecting investments for their clients. As a result, asset managers frequently rely more heavily on advisor-level engagement through wholesaling, education, and advisor events to drive product adoption across broker-dealer networks.

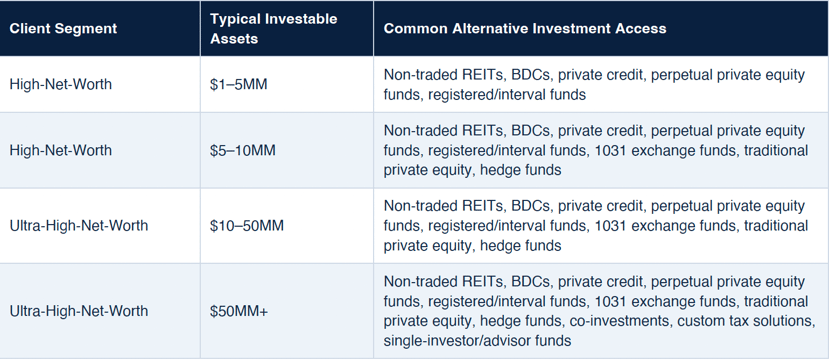

Expanding Alternatives Access Across Wealth Segments

Wirehouses have increasingly expanded their alternative investment platforms to serve a broader range of high-net-worth client segments. Historically, private market strategies were largely reserved for institutional investors and ultra-high-net-worth individuals. However, many wirehouse platforms now offer structured alternatives programs that allow advisors to introduce private market strategies across a wider client base.

For example, Bank of America’s investor day materials highlight how Merrill’s alternatives platform is designed to serve different high-net-worth tiers through a range of investment vehicles. These offerings scale in complexity and exclusivity as client wealth increases, allowing advisors to gradually introduce private market exposure as client portfolios grow.

Per Bank of America 2025 Investor Day Presentation - Global Wealth & Investment Management

In addition to expanding product access across wealth tiers, many wirehouses partner with their investment banking divisions and external sponsors to provide qualified clients with participation in company transactions, co-investment opportunities, and secondary market deals. By aligning alternative investment offerings with client wealth levels and suitability requirements, these firms are able to push adoption across a broader share of their client base while still reserving the most complex opportunities for the largest investors.

Outlook

Wirehouses and independent broker-dealers are both adapting to a rapidly evolving wealth management landscape shaped by technology innovation, shifting advisor preferences, and increasing client expectations.

Wirehouses are investing heavily in digital platforms, artificial intelligence, and integrated banking capabilities. Broker-dealers are expanding advisory capabilities and product access as they compete more directly with RIAs for independent advisors.

While industry structure will continue to evolve, both channels remain essential distribution platforms. Their advisor networks, client relationships, and expanding access to alternative investments position them as critical gateways to the growing wealth management market.

Dakota Marketplace

Dakota is a financial, software, data and media company based in Philadelphia, PA. Dakota’s flagship product, Dakota Marketplace, is a database of LPs, GPs, Private Companies and Public Companies used by thousands of fundraising, deal, and investment teams worldwide to raise capital, source deals, track peers, and access comprehensive data—all in one global platform.

For more information, book a demo of Dakota Marketplace!